Actually peak rates 🏔️🏦🌦️

Actually peak rates 🏔️🏦🌦️

EM without China, comparing private market returns, peak average, doomerism and Jeremy Grantham

Hi folks!

Let’s grab a coffee and get ready to close out this Q3 shall we?

The triple back-to-nursery, back to work and back to commute shock in our house seems to be (touch wood) be moving along just about ok, I’m still liable to start the day getting reprimanded by a 3-year old for cutting a banana the wrong way of course, but that goes without saying.

I think we’re at one of those funny seasonal moments where you’ve never dressed quite right - it’s going from 24 and sunny to rainy and stormy in a flash it seems. Expect those gillets and soft-shell jackets to be doing a lot of work come October though.

The dust has started to settle on last week’s central bank-athon, things have changed in the world of interest rates and maybe don’t mention the rugby to your Aussie friends?

Global stocks have fallen a bit and are down about 7% from the late-July high point but that’s little more than normal noise isn’t it and your global indices are still up ~10% year to date. A slide in sterling has helped out your sterling based global investors who don’t hedge.

It’s still all about those mega cap US stocks though, staggeringly as of earlier this week the Magnificent 7 were up 80% for the year while the equal weighted S&P 500 was slightly down. So whether you own those stocks in size or not matters.

Let’s talk rates as there’s plenty to say

I daresay if I looked back and did a search for “peak rates” in the last year of these updates there’d be a shed load of mentions, but, could we actually be there, for real this time? For long term investors one rates announcement here or there shouldn’t really matter of course, but key turning points do seem to have outsize influence on the long-term expectations, which do matter.

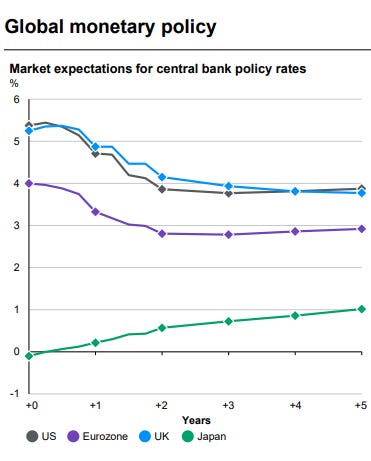

The significant surprise out of the big central bank meetings last week was the BoE who kept rates on hold but the most significant market moves were in the US where the market bought into the higher-for-longer narrative, taking market expectations of Fed rates a lot higher and raising the 10-year yield beyond 4.5%

These two charts from JP Morgan’s guide to the markets from 26th September (above) vs 30 June neatly show the big shifts in market expectations for rates in the UK and US, which have now basically converged together.

What this has meant is the yield premium that gilts enjoyed over treasuries ever since March time has disappeared and reversed. The market is no longer pricing the UK as a higher-yielding market.

Now it’s true that these market expectations have had all the consistency of a toddler trying to choose what to have for breakfast (why do we put so much emphasis on them again?), and right now I’m not sure anyone can predict UK rates with any certainty so expect this to change again but they do unfortunately matter for long term bond yields and so are important for allocators considering how to allocate their fixed income portfolios. How should we think about splitting allocations between the UK and US for example. The structural stable premia in the environment matter for long term allocation and right now it seems pretty hard to say what that looks like.

A widely-shared chart from Jim Reid at Deutsche shows that over a 200+ year history, the US 10-year is now bang on the average. It’s always odd to think of the current moment as average, as it never seems like it in the moment, but maybe that actually is the right way of seeing things now.

Three things I’m reading

Why you should consider allocating to EM ex China, a good piece by Jason Hsu who argues that China is too big a fish in the EM pond and to allocate more sensibly you should carve it out, that relies on EMxChina products existing though. (99+) Kicking the Elephant Out of the Room: The Case for EM ex-China | LinkedIn

Reported vs real world vs fair returns in private markets - very useful piece from PGIM, one reason you need to be really careful on compared returns in private markets strategies. Unfortunately this is far too often glossed over in the industry as I’ve written about before. Private vs. Public Investment Strategies: Reported and Real-World Performance (pgim.com) The headline is what you might expect but the details are just as important.

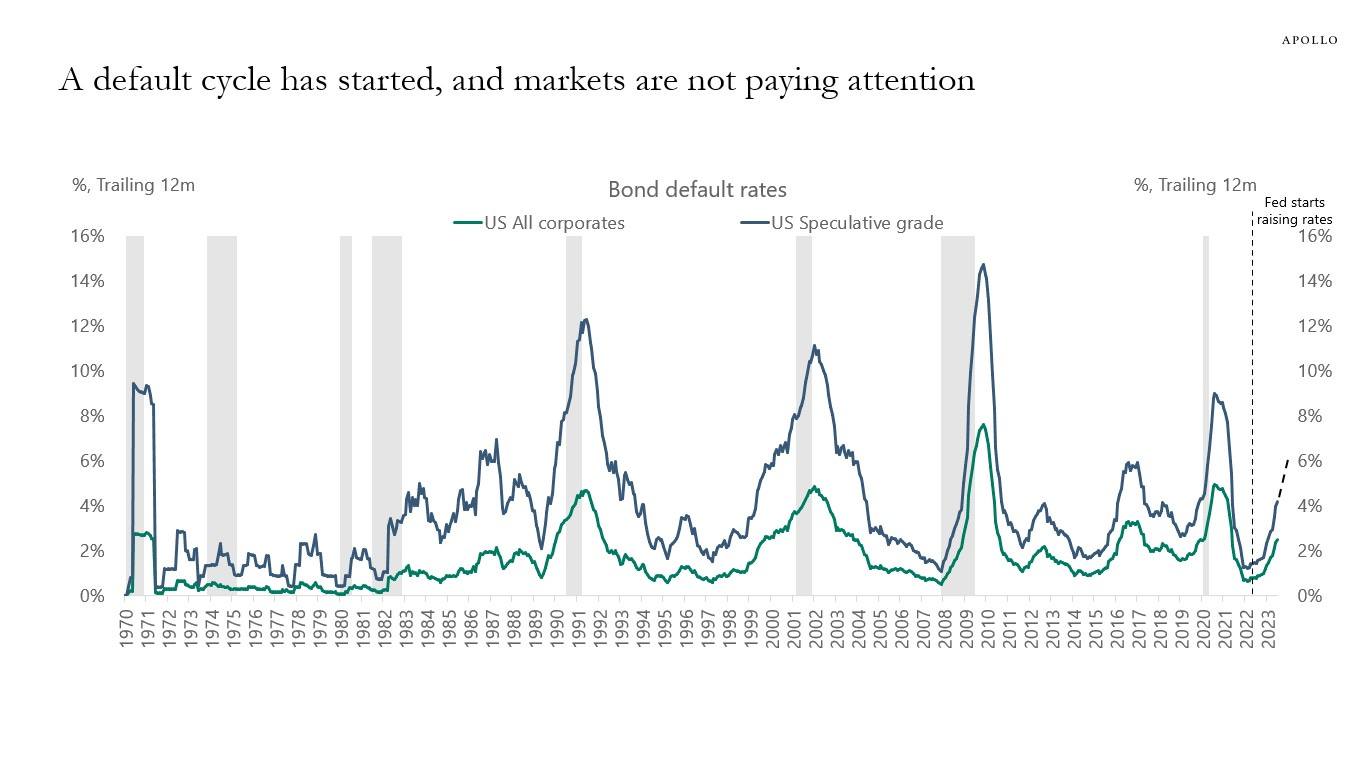

Are we at the start of a credit default cycle? Apollo think so, but has the credit markets noticed? - A Default Cycle Has Started - Apollo Academy

Two things I’m listening to

This new spinoff series from oddlots looks promising and is off to a good start with Neil Dutta

“Doomer folks say Hope is not a strategy and it sounds wise but really hope is the **only** strategy. Returns are usually earned before the resolution is clear” -

Great observation from Joe Weisenthal

It’s a super episode debunking financial doomerism

Almost didn’t listen to this as I’ve previously got a bit frustrated with Grantham’s tendency to constantly see bubbles everywhere (if I hear the one about the real estate in Tokyo one more time …) , and there is a bit of that but he is far more thoughtful than that and this was a useful reflection on valuation models, earnings, US equity and magnificent 7 dominance vs overseas. Plus a funny story about him investing personally in one of the bubbliest spacs ever and plenty on why we should worry far more about climate and environment risks. “The five most dangerous words in investing are this time it’s never different” and a great take on oil companies - “it’s the denial and the funding (of think tanks) that’s to blame here, not selling a product people want”

Grab bag

“Siri, time six minutes” … some interesting AI news this week as ChatGPT launches a voice interface and Spotify announces a collaboration to translate podcasts into other languages with synthesised versions of the hosts’ voices.

Right folks, we’re talking the big questions here, you get one setup forever, choose:

Have a great end to the week