Bear market over 🐻🎧🌞

Bear market over 🐻🎧🌞

The pause, peak rates, peak Messi, recency bias, diversifiers and defaults

Sheesh - this weather is coming in hotter than a Novak Djokovic second serve return out wide on the deuce court. Grab me an iced coffee.

While I was holed up in an Edinburgh conference centre last week some real stuff was going on in the world. There was this crazy wildfire smoke in New York, Apple released their VR headset, Boris Johnson left parliament, Lionel Messi signed for Inter Miami, the SEC decided it wants to end most of the crypto markets and of course the Ukraninan counteroffensive began.

We spent a good part of the week though in this cool little space speaking to an array of the biggest investment decision makers in UK pensions. The content is worth a listen for anyone who wants a quick 360 degree pulse on the whole UK investing space in the time it takes for your weekly commutes.

You can catch the episodes here: day 1, day 2 and day 3. All of them are on apple and all other good podcast apps. Some big questions on investing in the UK, communicating risk well and revisting beliefs that have become deeply embedded at times of regime shift. And why seeds … yes seeds are the new conference merch of choice. Fantastic news for the herb garden.

Three days in person at a conference is a lot, but I really can’t see VR headsets replacing all that anytime soon, it was wonderful to see people.

I reckon June is like the Friday of the summer months, so before all those Friday afternoon vibes get too strong there’s some markets mumble to get through:

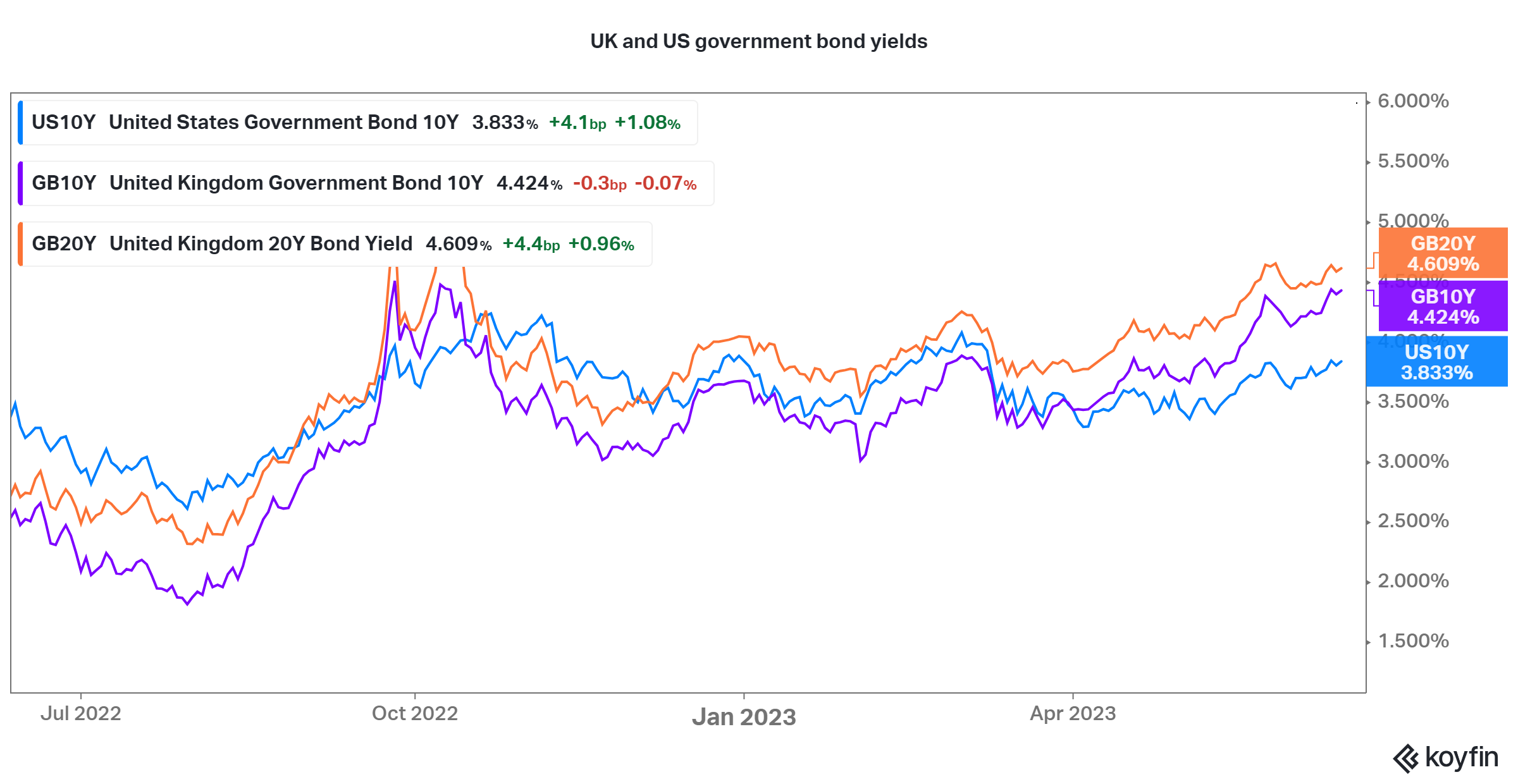

US inflation, probably still be biggest single data point for global markets declined as expected to 4% this week (although there were various devils in the detail). The Fed followed up by holding rates steady yesterday. John Authers sums this up by saying that the inflation scare of 2022/23 is now entering its final phase.

But has it peaked?

Markets have pretty much now removed those long priced-in rate cuts later this year, athough market expectations for the Fed funds rate still fall a little short of what the Fed published in the dot-plot, which has a couple more hikes in there before the end of the year. UK peak rates have been pushed right back up there to the high 5%’s.

Goldmans have revised down their US recession probability to 25% (link). They’ve always been well below consesus on this one:

You can still read the data whichever way you like though - some popular indicators such as the conference board’s leading economic indicator, and other survey-based data points are very much still flashing recession.

As for markets, stocks have staged another little surge in June, up by around 5% across the board (other than the UK) as the market moved to expect the Fed to pause the hiking cycle this week. For a number of the major indices (World, US, UK) this takes them well over 20% up from the lows, which, legend has it, signals the end of a bear market and the start of a new bull market (whatever that means).

Some are calling it the AI-rally, which I think is a little simplistic to put it mildly, but we can add that narrative to the soft-landing, hard-landing, credit crunch narratives that have all been tried out so far this year. It’s a bit like living through the entire 2000’s in one year but with worse music.

Your global stocks are now up about 14% for the year (in dollars), about 8% in £ unhedged. The Nasdaq is still storming ahead with Apple hitting new highs (up 40% this year), and Microsoft, Amazon and Alphabet all up more than 40% too, + Tesla, Nvidia, Meta and Netflix all up more than 100%.

Japanese stocks are having a moment - threatening to get within shouting distance of those 1989 highs for the first time in 30 years, while fully half of the Japanese stock martket trades below book value says Duncan Lamont. Buffett seems to like it too.

Emerging markets have also had a bit of a boost and are now up 8% for the year.

Rates are up, particularly in the UK where the sticky inflation problem we spoke about last time looks to be really real.

Good fortnight for -

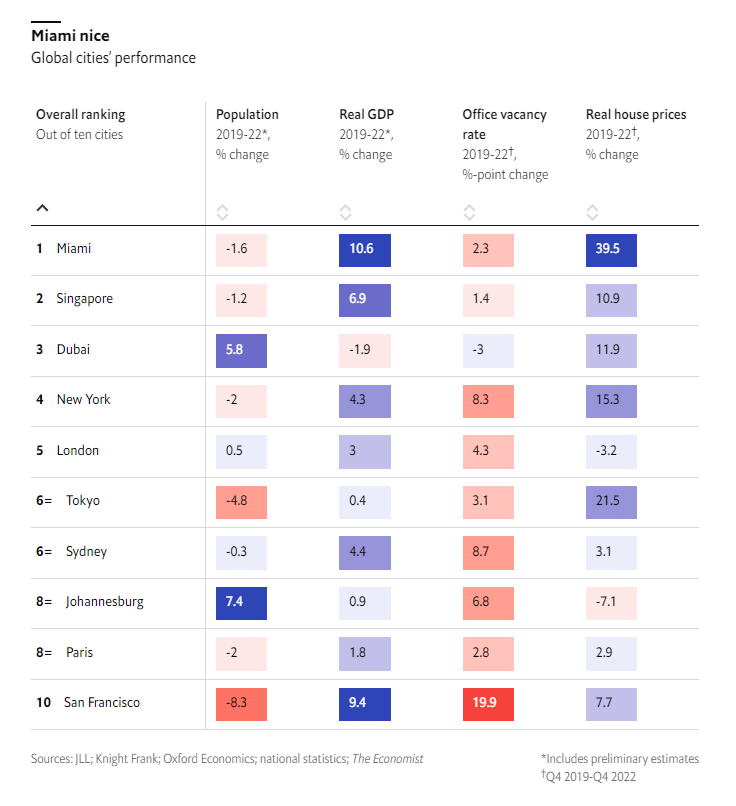

Miami. Well, although they lost the NBA finals they have reportedly snagged Lionel Messi in a deal that (in Michael Jordan style) reportedly includes a cut of apple TV subscriptions, a share of Adidas sales and an equity stake in the team. Messi’s market cap is definitely hitting new highs. The economist also ran an index tracking the 3-year perfomance of global cities which Miami tops -

Bad fortnight for - crypto and hashtags. Marrying couples are no longer prioritising finding a wedding hashtag, apparently. I think conference hashtags are also dying a little bit. What was really he point.

Three things I’m reading

1. Investors, drop your recency bias says Karen Ward in the FT (link)

This is sound advice for all allocators and resonated a lot with discussions in Edinburgh at the PLSA investment conference where the sme topic came up again and again.

The easy bit is talking about it though, the hard bit is actually doing it because it’s so hard to actually see where the recency bias is manifesting itself. Stable features of an enviornment like the last decade can get built quite deeply into frameworks, models and systems of thinking without even realising it.

What I think Karen is getting at here isn’ simply a question of “stocks will go up/down” but structural features of markets implied by low and stable vs high and volatile inflation that have real consequences for long-term allocation like stock/bond mixes and the existence or non-existence of various premia attached to asset classes.

Could the US dollar be a better diversifier than bonds - Wisdom Tree’s Jeremy Schwartz (link)

This has implications for the currency hedging programs of all (non-US) investors if so …

Picking up on Karen Ward’s point above - this is one of those structural things that might need to be re-evaluated in a new regime.

Bed bath and beyond isn’t the only company that has thrown in the towel this year - Tupperware and more have also had their fate sealed …

But defaults are only creeping up from low levels at the moment. An abnormally low issuance in high yield could be keeping spreads low.

Two things I’m listening to

Goldman are not seeing big evidence of deglobalisation in investors’ portfolios … yet (link)

Grab bag

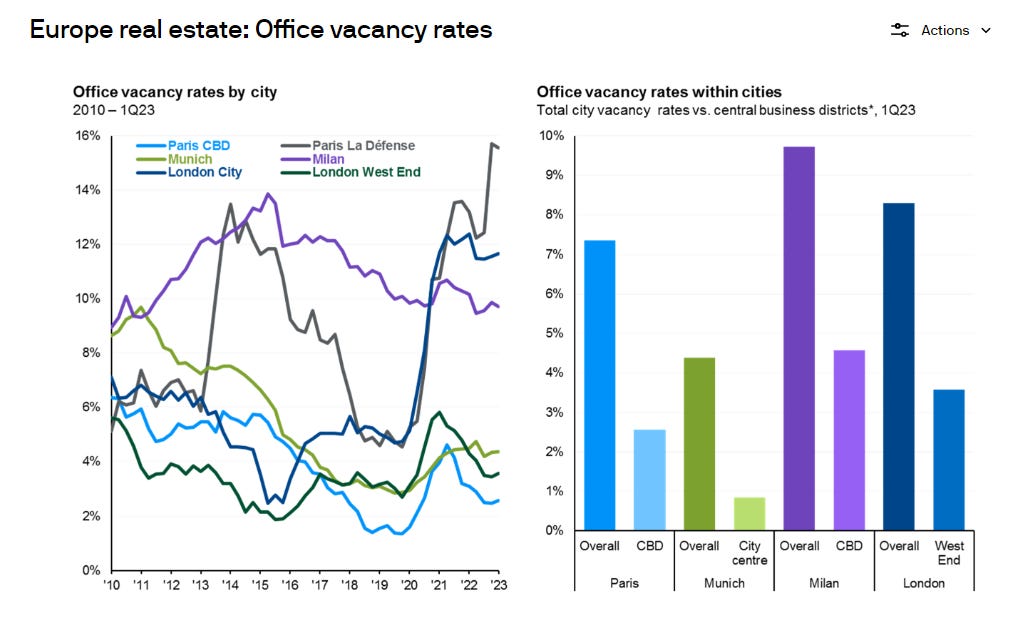

I liked this chart in JP Morgan’s guide to alternatives on office vacancies. Typically the message on vacancies seems to be they are higher in many US cities, but in Europe it’s different with the likes of the City seeing much higher vacancy rates but the West End fairly low.

BCG has the total AUM of the global asset management industry falling 10% to $98 trillion over the last year.

Mark Andreessen has a strongly bullish take on AI.

Finally, quick bit of personal news …

Have a great fortnight, till next time