Bulls are back 🚀🐂🐃

Bulls are back 🚀🐂🐃

LDI redux, new news, a smart beta beef, the IC chair and Tesla's valuation

I read somewhere that February arguably has the best start to end improvement of any month: you start with all the frost and bleakness of January but ends with snowdrops, daffodils, birds singing and half a chance of getting home in the light - I like that take, don’t know about you but our flowerbeds badly need some spring vibes. And of course … we have 6 Nations rugby back. Not a good result for England fans, but I must secretly admit I’ve enjoyed watching a few replays of **that** Duhan VD Merwe try - has Twickenham ever seen a better score from a visiting team? You probably have to go back to Saint-Andre in ‘91 (link)

Now who knew toddlers have such strong views on the suitability or otherwise of slippers in the mornings 😅

New news for markets last week ended with stocks doing backflips, and the bulls out in force but there’s details.

Before we get started - awful news to read this week on the quakes in Syria/Turkey isn’t it. And the headlines just seems to keep getting worse, a terrible time for those people. Donating to the The Disasters Emergency Committee (DEC) charity is one small way to help (link). No easy way to pivot from that but …

First, more this week on LDI - and I have thoughts:

The letter from the Lords committee (link) makes slightly painful reading for investment consultants let’s be honest.

LDI is painted as short termist, and a response to artificial accounting requirements - I think they’ve run with that argument a little far and the “short term” label grates.

Is the term “accounting” getting a little confused with “financial measurement”? They aren’t the same but framing as accounting invites folks to look at it all as artificial. As I mentioned in my long read on the history of LDI that got featured in the FT, one of the key planks to the whole thing was a key paper on the Financial Theory of Defined Benefit pension funds. It really was never only about the accounting.

But sure, if the answer is better systemic regulation, a refresh of accounting regs, asset led discounting, and even regulation of consultants then fine - no issues with that.

And it looks like late-March is going to be an important date for this new steady-state framework from the bank. Mark your diaries!

Markets mumble from the last two weeks, it’s been busy. A story in 3 parts and what it means for asset owners.

John Authers column (here) is the place to go for all the detail, and you’ve read all that already so let’s keep it short and get to the so what …

Part 1: Central banks announced a bunch of rate rises. In contrast to what they were actually saying and doing, markets felt that Jerome Powell was giving off a strong “inflation is really falling and rates are peaking” energy. And stocks love to see it - particularly tech. It has to be said that mood music and body language analysis was doing a lot of work here.

Part 2: Three of the world’s biggest companies reported earnings, quartr has a superb little recap (here) and these results definitely weren’t “wow” and were probably worse than “meh” - revenues were flattish to down (hello search & YouTube ads) but much of that was FX effects. Overall maybe not quite the kind of super super ugly that would make you think a big economic shock is coming. But John Authers thinks that big tech is “getting away with it” in market reaction to bad earnings. Amazon and Google stock have seen multiple 5% up/down days in the last week which gives you some idea of the gyration out there.

Part 3: US jobs data showed that - to everyone’s surprise - lots and lots of people are getting jobs and very, very few people don’t have a job. This is very far away from what would happen in a recession. But a booming economy means higher rates. If markets were screaming “RATES HAVE PEAKED” on the Thursday, they were whispering it a little quieter come the weekend.

At the time of writing the main developed markets are flat compared to just pre the central bank announcements, tech is up and EM is down. And of course the UK market has hit a new all-time high.

Make it make sense! What does it all mean? In a “good news is now bad news” plot twist, the jobs data took a little of the shine off the surge higher in stocks we’ve seen - this hurt all stocks but particularly emerging markets that have done well on the back of the lower-US rates and lower dollar story. The question for investors is always: how much has the world really changed, and what does that mean over the medium and long term.

The two key competing narratives here seem to be whether (1) the market is currently banking on a perfect “Goldilocks” scenario of falling inflation, peaking rates and no recession which is quite unlikely or (2) whether the macro backdrop actually **is** becoming pretty supportive for the start of a new bull run in stocks with the big interest rate and inflation surprises of 2022 behind us and recession less likely. My instinct is toward the latter, I think it’s easy to get trapped into always worrying about the former. And I think “good news is bad news” is the sort of noise asset owners need to look through: good news is good news over the timeframes investors ought to care about. But the market is sure going to be trying out both explanations multiple times.

So yes, your stock and bond markets are up for the year with tech and EM going in different directions over the last week -

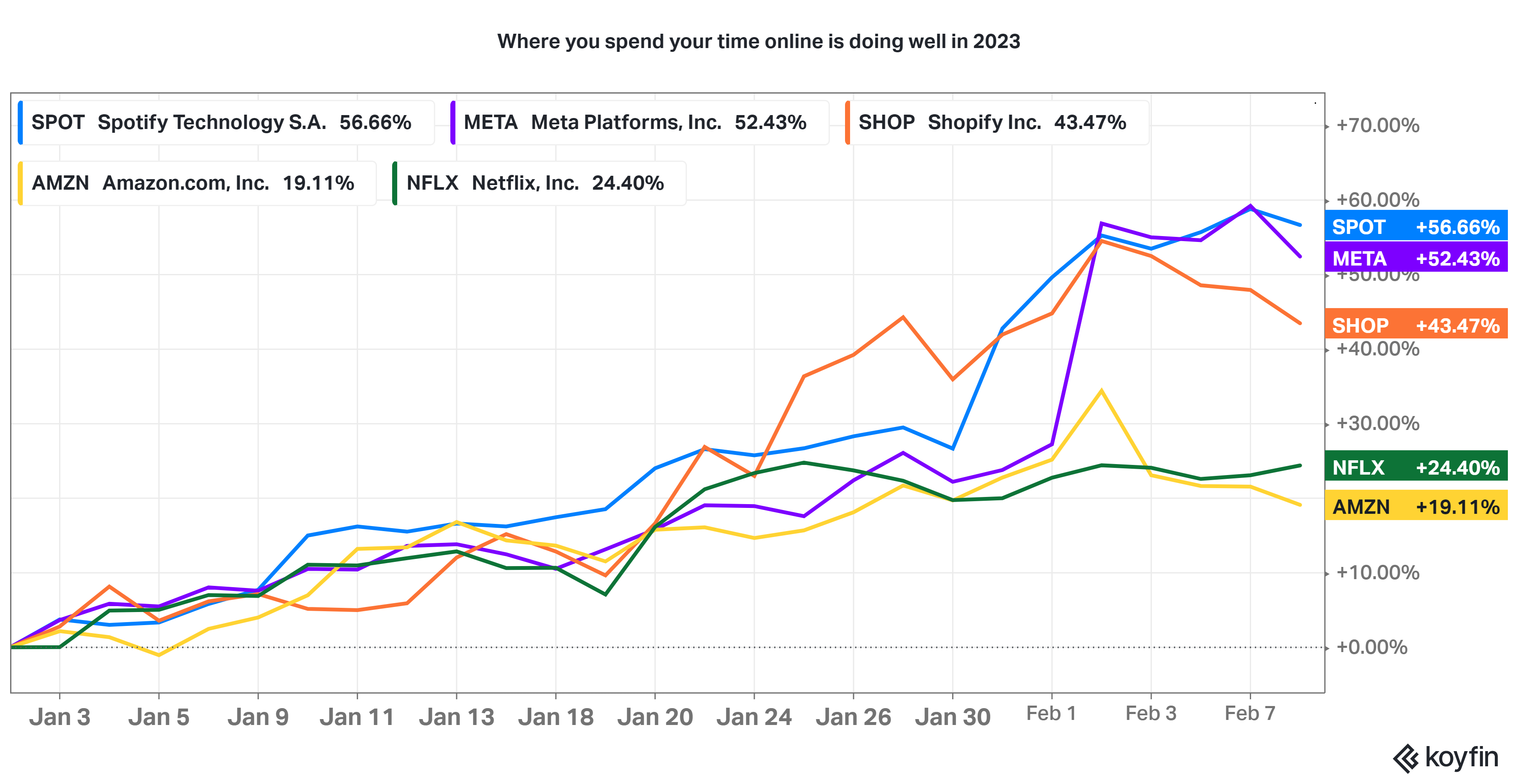

The index of where you spend you time online is doing really well (Meta, Shopify and Spotify all up +40% ytd), some might call it a trash rally, I think that’s being a little unkind - these aren’t exactly meme stocks or crypto exchanges are they?! but the rally this year is being led by those sectors that had an awful 2022, communications being chief among them.

Three things I’m reading:

Continuation of a useful back and forth (one could call it a “beef”) on one of the thorniest questions for allocators: should you overweight factor strategies?

Revisiting “that” Horribly Wrong paper - Research Affiliates (link)

Research Affiliates and Rob Arnott are here to remind us they did a piece in 2016 warning that smart beta factors were potentially “overvalued” due to crowding (link) and subsequent returns could be bad. They were. So they are taking a little victory lap here.

They revisit these valuation judgements concluding these factors are now favourably valued pretty much across the board from value to low vol to quality in the US and emerging markets.

Not so fast say Cliff Asness and colleagues at AQR (in a long piece which also touches on a bunch of other important factor questions) - (link)

AQR think there’s little to be gained by trying to time factors. Just buy and hold. Even that is easier said than done after the ride we’ve had. On timing, a factor is a constantly changing basket of long (and short) stocks, it doesn’t make sense to think too deeply about the “valuation” of that thing. The AQR piece is long and looks to mythbust on a range of other points including: are factors data mined and crowded (no) and does factor diversification go wrong when you need it most (also no).

Why it matters (1) This long-running debate between two giants of the field touches on a perennial challenge for allocators that goes beyond smart beta: can and should you try and add value by over and under weighting different strategies?

It’s certainly tempting, but AQR’s reasonable pushback is that you are gonna want some kind of evidence that your “valuation” metric has helped returns in the past. Often that’s not there - even in very familiar and static areas like price earnings ratios and equity markets, much less in the dynamic nature of factor baskets,

(in RA’s defence, they **do** think the evidence is there - what they show doesn’t exactly seem compelling to me - but here’s one other key nagging issue with this debate, there’s disagreement over core facts. I’m not sure the two sides even agree on how individual factors have performed).

Why it matters (2). Also a really important behavioral point. Drawdowns in stocks are generally tolerated as folks are pretty confident they do “work” over the longer term so they have this faith to stick with it, whereas drawdowns in “other stuff” leads to myths or misunderstandings (or career risk) that dent investors’ faith more easily leading them to give up at bad times. Everyone loves a diversifying asset until stocks are up 10+% and your asset is down or even flat, so maybe there is a practical limit in the tracking error you can allow from stocks.

Thought bubble. I still think managers often swerve a couple of elephants in the room when looking at that dire period for factor returns: the influence of that tech index reshuffle in 2018 in breaking all the backtests and the impact of the short side of these trades on the overall risk profile. These aren’t fundamental doubts about the approach but more implementation practicalities that do really matter.

Yes, but. AQR address these a little under #3, the fiction (as they see it) that diversification failed when you needed it most. You need to understand that one single factor can and will dominate performance over short periods, maybe at the worst possible time. So as an asset owner you need to be really careful about how you think about this. My one quibble with AQR would be are they putting too much back onto clients here? It’s a little much just to say look factors are risky deal with it we never said they were magic. There’s responsiblity here on the asset manager too to help their clients size this right.

Between the lines: To get a little geeky for a second the difference between long run and short run correlations really matters - and it can be tempting to focus on long run but this may be a mistake based on what we learnt over the last few years, the long run is all very well but it’s the short run that’ll really hurt you. The issue is that if you think you have five uncorrelated returns streams when you put them together in a model it looks like unadulterated magic and unless you are very careful you set yourself up for disappointment because nothing is magic.

The Research Affiliates piece also goes to another really fundamental point - really really weird stuff can and does happen in the markets. They had to totally rescale all their charts to cope with the valuation metrics from August 2020. Granted, this was a super-weird time but that’s the lesson - things will get far weirder than you or your risk model think for far longer.

Both the pieces are long, and I’m well aware this is a long running debate so I can’t possibly do justice to all the issues and the putbacks to the putbacks, go read the pieces yourself!

The Unheralded role of IC chair (link) John-Austin Saviano

This is a great little paper on what I agree is a vital but often overlooked role in he whole investment piece.

some highlights:

Agenda Setting

Many sins of governance happen in writing agendas. Deciding what will be focused on, by whom, and for how long is fraught with opportunity for misstep. The IC Chair must keep the whole enterprise focused on the right things.

Time Horizon

To paraphrase Mike Tyson, “Everyone is a long-term investor... until they are behind their benchmark.” … Keeping everyone focused on years and not quarters is an essential role of an IC Chair.Renewal

A Chair is responsible for initiating and guiding self-renewal for an IC.

The agenda point is maybe the one that most resonated with me - it’s the most influential thing that I don’t think we recognise often enough.

Any thoughts on this from the IC chairs out there?

Two things I’m listening to

Aswath Damodaran is taking pushback on his Tesla valuation ( youtube )

He did a full DCF (disclosing assumptions - web | spreadsheet ) and came up with a fair value of $130 (equivalent to a market cap of $400bn). That’s some way south of where the stock currently stands (around $200, but it was sub-130 till mid-Jan), but the surprise maybe is how close this DCF is to value is to where the stock has traded not long ago.

Predictably enough both the bulls and bears were out for him on this one, but overall a worthwhile and interesting lesson I think in what goes into stock valuation.

As he says, the best companies to value are not the easy, predictable companies because anyone can do that. The best return on valuation skill is in the hard to value ones.

Really useful and insightful conversation this one on trend strategies (one of few asset classes that did well last year), a few takeaways:

It was the real “basic” trend following models that did best in 2022 (the bells and whistles and risk control didn’t help returns)

Is trading edge still possible - and how’s it changed over 20 years

What drives trend following: Information propagation in markets, autocorrelation and behaviour

Does the quant industry focus too much on sharpe ratio?

How to evolve a quant system through time: tweaking a trend system doesn’t make much difference, but adding markets does.

Are there too many trend followers, and how you’d be able to tell in the returns

Grab bag

Back to the 6-nations I’m a big fan of the bbc rugby union weekly/daily podcasts (web | apple ) with Chris Jones, Ugo Monye and Danny Care, it’ll give you all the talking points and hot takes you need for a Saturday in the pub that you can easily re-purpose as your own. Get your thinking sorted on the merits or otherwise of the Smith-Farrell combo for England and even the new tackle laws. Ireland / France this weekend is going to be huge. But of course England/France on March 11th is the big one in our household: the boys have both England and France kits, and I imagine negotiations will open soon on what the allegiances will be.

Our podcast with rock star actuary Stuart McDonald MBE is out - we’re talking Health in the UK and how Stuart arrived at the awful but important 300-500 deaths per week figure that led the front pages a few weeks ago. (Web | apple )

Linkedin hits 900 million users. As I like to say, come for the humblebrags, stay for the analysis 🤣 Forget the haters, Linkedin reach can be huge. Follow these accounts if you want some inspo.

These visualisations of population density are pretty beautiful aren’t they, and well as quietly insightful (speaks to history, cultural centre of gravity and tendancy to centralization). link to Visual Capitalist for more.

Have a great rest of week all, stay warm!