Done hiking 🏔️🌷👑

Done hiking 🏔️🌷👑

Fed pause, earnings good, ESG seachange, Black Scholes at 50 and power dressing

Good morning from the newsletter coming at you with all the excitement of a toddler who just spotted a dustbin lorry reversing …

My bbq excitement of two weeks ago ended up being a little bit of a false start given how unreliable the weather has been since then, but every ray of sun is to be cheered at this time of year right? There is hope - our flower bed is starting to show signs of life, and my herb garden has really come through for me. The Rosemary is fragrant, the Chives are flourishing, and the Sage is stronger than ever. But, let me tell you, the crown jewel of the garden is that Parsley … who says you shouldn’t plant herb gardens in November … score one for the contrarians.

Now, brace yourselves for this one - we went to the cinema last weekend for what we think was the first time in seven whole years! It was totally worth the wait. We saw AIR - a great film with a captivating story. Plus, we're both huge fans of the book Shoedog. You won't believe how emotionally invested you'll become in the story of a shoe (but of course it was never “just” a shoe … ). Plus, Ben Affleck as Phil Knight rocking the 80’s shellsuit plus wraparound shades is just a whole vibe

Kinda boring though?

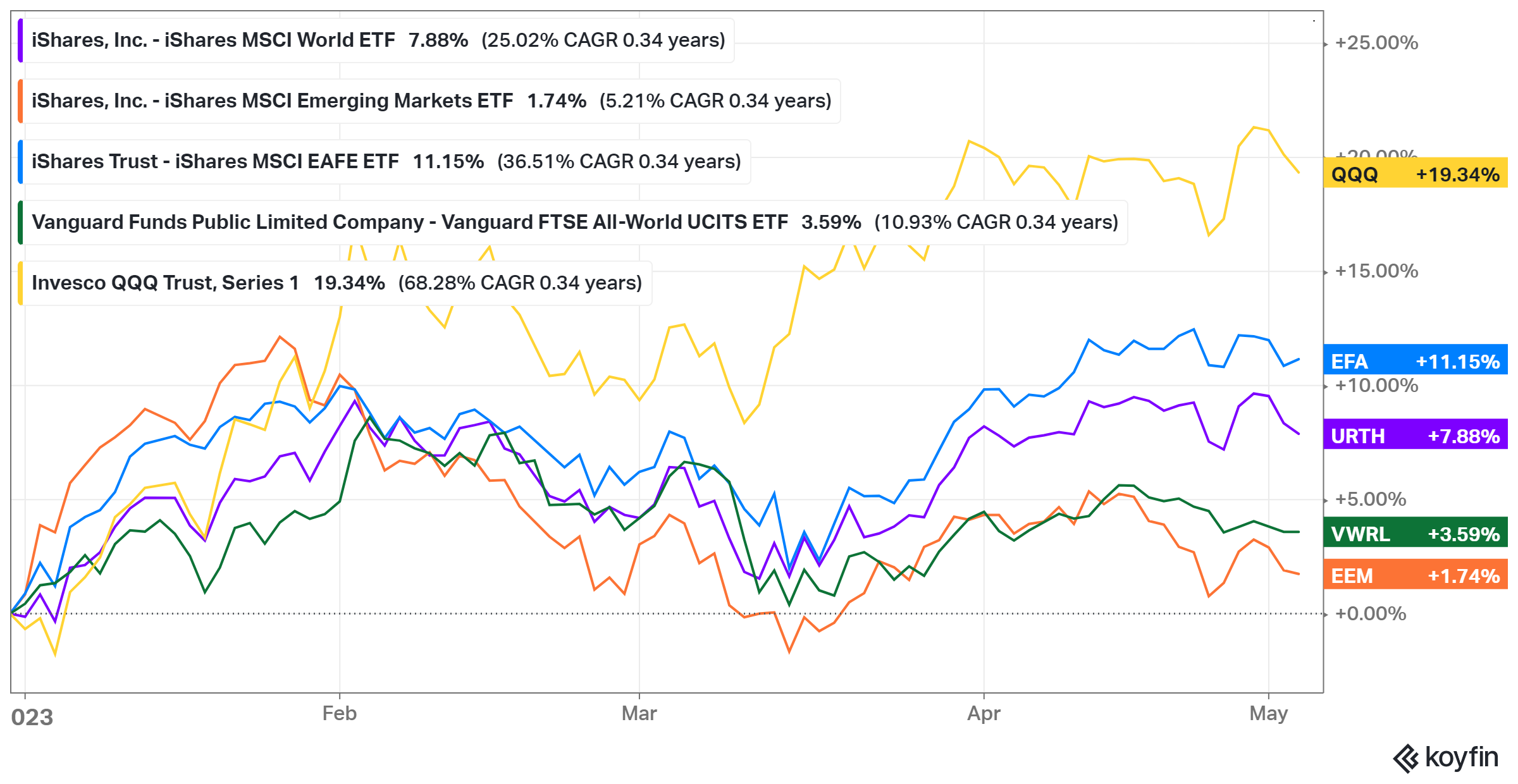

No slam dunks in sight. We might just have entered the yawn zone of this market. Sure, there's been new news on earnings and rates, and some action in the regional banks. But overall, the market isn't exactly blowing our minds. Stocks ground about 2% higher in April up now 8-10% ytd (your usual charts below). Even Ben and Michael on Animal Spirits seemed unusually short of stockmarket related talking points this week.

In a nutshell: the Fed is probably done hiking, earnings are pretty good and markets are a bit boring.

Diving in: the main macro themes as I see them continue to be

The rate rise cycle - yesterday’s Fed hike could be the crowning achievement of this cycle, which the market thinks is the last one, while there’s probably further to go in the UK. One standout observation continues to be the market still pricing substantial rate cuts by year end. How plausible is that really though?

The main takeaway for long-term investors is the return of yield, higher rates are giving short dated high quality bonds an excellent head start on returns (and a headwind for asset classes that use leverage). More on the return of returns here. Longer term markets expect rates to settle around 3%.

The US economy, which is slowing slightly and the labour market loosening a little while not showing any of the key signals of a recession.

Earnings - in more new news in the last fortnight the earnings season was actually pretty good. Per Wisdom Tree’s excellent tracker US stock earnings surprised 8% to the upside and sales by 2%. Why?

Excuseflation. Think Macdonald’s think Pepsi: both have been able to raise prices, both have seen their stock jump to new highs. Sure grates a little when a lot of folks out there are really struggling but there you go.

That’s feeding into that new bar on JP Morgan’s usual chart (RHS) which now shows earnings growth in 2023, driven by margin expansion. Future expectations are getting revised up a little bit. Has the earnings recession been and gone?

For long-term investors the US market is really where earnings growth has been for the last decade, and that’s been well rewarded but that’s why it trades on a much higher price-earnings multiple than the rest of the world. Will that be repeated in the next decade or are we finall due a comeback in Europe, Japan and Emerging markets?

Markets -

European stocks and US mega-cap tech are having a moment here.

Main indices are up 8-10% ytd, but emerging markets are only +2%, and an appreciating sterling means UK unhedged returns are lower than the $ numbers.

Divergence between US and UK rates continues

Three things I’m reading

The Ruffer Review - Gone with the win win Daniel Austin (link)

Explained: I slightly reject the starting premise that ESG is founded on the ethos of win-win ism, but what he is effectively saying is a need to move beyond seeing ESG purely as a financial risk thing and to look at impact and now see it grounded in moral rather than financial obligation.

Between the lines: but he grounds it all very much in free-markets type theory, essentially he runs the argument that missing costs of externalities like pollution are a huge market failure that will prevent markets coming up with a good solution (unless they are internalised)

He argues that free-market thinking got too much primacy on the back of simplistic and flawed, but "neat" models, and now a lot of that is institutionally locked-in.

And he has this lovely extension of the classic Adam Smith free markets viewpoint: really worth a read

A metaphor may help fix the intuition. Essentially, we are discovering that Adam Smith’s invisible hand is connected to an unmentionable foot. The hand represents the market’s autonomous allocative and innovative dynamics, which are real and remarkable and have been much celebrated. But the foot represents the real costs generated by market activity which are not recognised and land on other people and other places, sometimes with a lag.

Unfortunately, the hand and the foot are engaged in a dynamic struggle. A market system’s overall benefit for human wellbeing depends on the relative strength of the hand’s (internal and recorded) value creation and the foot’s (external, largely unrecorded) cost-shifting. To believe that economic growth can solve all social and environmental problems is to trust that the invisible hand can always repair what the unmentionable foot damages – and do so before irreversible or intolerable harms occur

I think this is a fair statement of where ESG thinking is at - other folks have said similar so I don’t see this as ahead of the curve. The issue is that concrete actions are still seen as being needed to be rooted in beneficial financial impacts to gain any traction and the case for a morally-driven agenda has not been landed broadly enough (yet).

The problem with UK capital markets - Simon French (twitter)

Great thread which gets at the complexity of the problem and the key question for asset allocators - is the discount a permanent feature or cyclical?>>

It feels a little wrong to be dwelling too much on British declinism in the week we’re all going ga-ga for the coronation, but it’s practically it’s own field of literature right now and that’s partly the point says SAMUEL MCILHAGGA (link) who is here with a scorcher of the genre. Britain has been dining out on the soft power of yesteryear while doing little of real use while the ruling classes rent-seek for over 100 years. He charts the genesis of this back to the absence of a re-founding moment, grounded in industrial progress like those in the US and France.

Black Scholes at 50 - how a pricing model for options changed finance (link)

This is a very good little explainer on Black-Scholes and the impact it had on option pricing through the 80’s, 90’s and beyond.

I look back fondly on a chapter of my career spent coding up Black Scholes formulae into Matlab, and I’m with the author here that the equation became “performative”: its practical use shifted reality towards its predictions. This changed a little post-1987 as the vol smile/smirk emerged, but the equation remained strongly in force as a way to translate price.

Two things I’m listening to

Professor John Y Campbell on Rational Reminder: Financial Decision Making for Long Term investors (web | apple)

A whole load of good thinking points in here:

If interest rates are countercyclical (2000-2020) then bonds and stocks hedge each other: 60/40 is King. If interest rates are procyclical (eg 1980s) then that changes the game to a positive correlation - implications for asset allocation

We could be moving back into that sort of regime

Decomposing beta into “good” beta and bad beta gives another way to think about value vs growth

Only half of year to year stock volatility comes from changes in earnings potential for the companies

Currency hedging: think about the tail correlations of your currency exposure with the underlying investments - the dollar can be a great tail risk hedge

Wherein two big-name advocates of the secular stagnation / lower forever thesis, Olivier Blanchard and Larry Summers are now going different ways with Summers getting firmly into the rates-higher camp but Blanchard seeing this as a temporary blip in a lower rates world.

Grab bag -

On power dressing

Succession episode 5 was a power dress-off in the Norwegian Fjords which

breaks down brilliantly on her substack. It set the Roy family’s Bruno Cucinelli puffyvests and Ralph Lauren Houndstooth vibe against the everyman Fjallraven outerwear & chunkyknits of Swedish entrpreneur Lukas Mattson & his cool crew. Odell identifies that Matsson (played by Alexander Skaasgard) successfully deploys his "aggressively normcore" style in becoming pretty much the only character in the show able to consistently gain the upper hand in tension with the Roy family.If like me you’re chomping at the bit to get at the weekly drops of Succession episodes then a strong recommend to keep you going in between is House of Gucci (Amazon Prime). This ramps the power dressing and power-play game up several levels all set in 80’s and 90’s Italy with the best fake Italian accents you’ve heard since The Death of Gianni Versace. It also has an excellent nostalgia soundtrack (spotify link). The Tracy Champan/Pavarotti duet that closes the movie’s final scene is just sublime (Spotify).

Stacy Havener was kind enough to invite me onto her new podcast (apple) so I talked all about: the problem of conformity in asset management, what really stands out and the real consequences of the move from stocks to funds. Have a listen!

London is getting older -

John Burn-Murdoch, the crown prince of data viz strikes again -

Two key drivers not surprisingly are seen as housing and Brexit, with Ian Mulheirn, also adding some good angles

The net effect is that London is becoming older and less cosmopolitan. Housing policy needs fixing. But it’s Brexit, not housing, that’s killing the capital.

Enjoy the long weekend folks, till next time!