Euro fever ⚽️ 🏆

Euro fever ⚽️ 🏆

Market disconnects, the economist hot take on ESG, good losses, busy fools, expected returns & pre mortems

Who’s excited for the big euros final! Just please no penalties 🙈. Commonwealth games also kicking off today in Birmingham.

New technical economics term just dropped - StagGrowth: It's like stagflation, but with better growth. All the indicators are good but everyone agrees the vibes are like, iffy.

It might feel like half the world’s wound down for the summer but this week has been a busy one for new data points on the big questions of the moment (are we in a recession, where will the Fed funds rate peak, are company earnings still strong and what’s priced).

Stock markets seem to have reacted positively overall continuing a mini rally so far this month of 6-7%.

The Fed’s interest rate decision came in as expected, and although there were a few earnings shockers (hello Snap, Walmart) there were enough positive , or at least not bad, results (eg Google, Microsoft).

People are really hating on instagram trying to become like TikTok. But is it really just a response to how we’re all using it?

Bond markets are starting to dial back inflation expectations.

Kristin Hooper talks about five disconnects that are perplexing people in the current environment in her (excellent) weekly newsletter): on recession indicators, inflation, the consumer and european monetary policy.

Are we in a recession? Ben Carlson sums it up:

3 things I’m reading

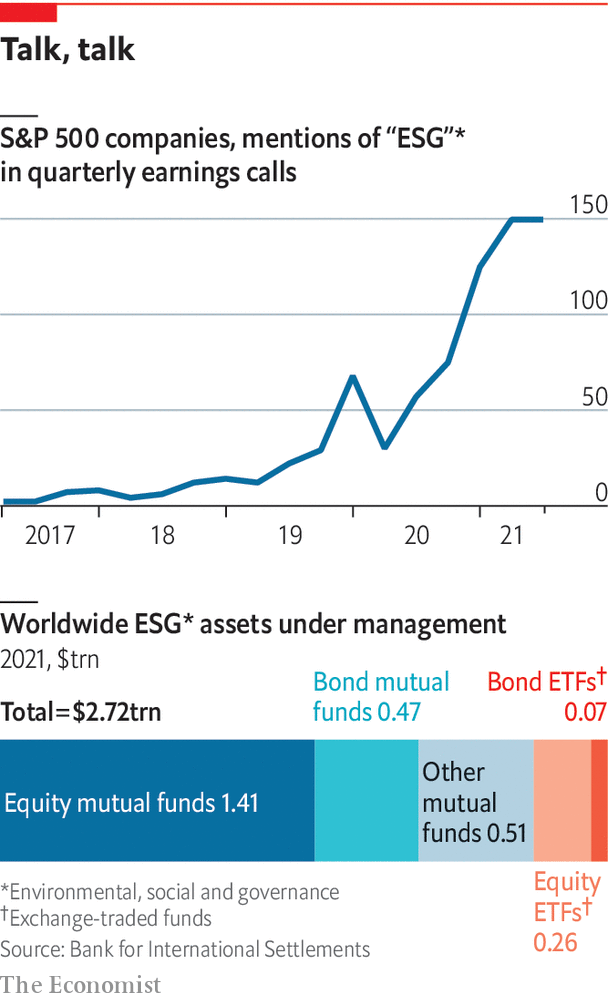

The Economist has written a critique on ESG. It got quite a lot of (generally sensible) discussion going on LinkedIn. They also did a good podcast that summarises the main points (listen here).

Here’s my take. Usually I eye-roll at the ESG takedowns, they’ve become predictably formulaic: set up some weak, fake strawman of how ESG works to tear down, employ superficial, naive levels of understanding. set up some impossible goals that ESG never said it was trying to achieve to evaluate against. Usually it’s done by folks who don’t get that things need to change, or actively don’t want to get it (hello Warren Buffett , Charlie Munger etc) .

But the Economist piece manages to rise above a lot of this, makes some correct diagnoses and offers real pragmatic approaches to go forward.

Let’s start with what the economist gets right:

- ESG is a hotbed of greenwashing (true - wrote about this here)

- ESG is a platform for flogging expensive funds based on flakey ratings (true)

- ESG contains a myriad of pointless, boilerplate terms (“ESG integrated”)

Solution?

The Economist says: Focus and measure less, but better. Maybe even make it all about emissions.

I think I half agree with the solution

But it shouldn’t all be about focusing on data and better more reliable data. Part of the reasons ESG needed to exist was not everything that matters can be crammed into a spreadsheet. That’s the issue. So trying to make it all about data isn’t the answer.

Frameworks can exist to make decent investment decisions in the absence of perfect data

(Indeed that’s what investing is really all about. Come to think of it a lot of the “data” we take as golden, company earnings for example (see below) is no where near as robust as we like to think. In just one example it was found that the data on share volume traded for one of the biggest companies in the world (Berkshire Hathaway) for last year was complete rubbish. People use that stuff.

Zooming out: ESG used to struggle for airtime and relevance, it’s a step forward that it’s central to the discussion and not an afterthought.

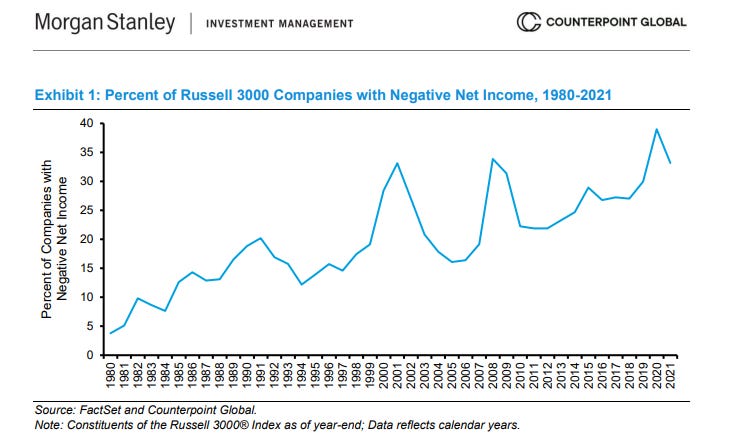

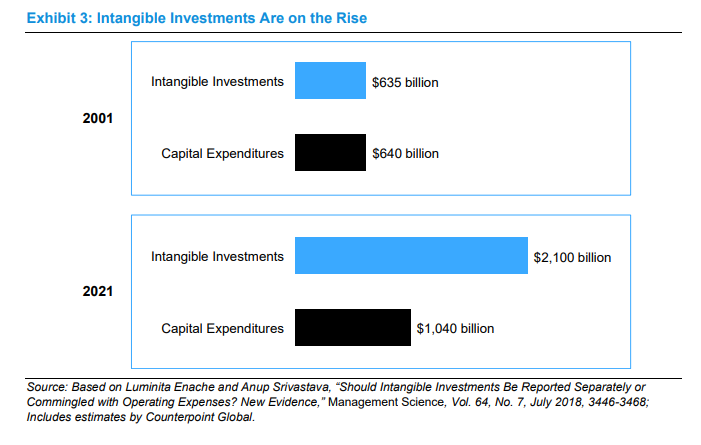

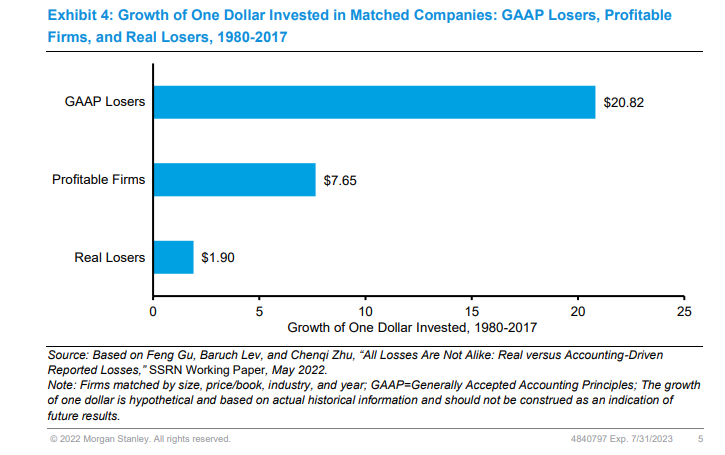

2. Good losses / bad losses. The rise of intangibles has totally reoriented the world of investing and accounting practices are decades behind how firms operate and what drives value in today’s world.

So what? One consequence of that is in profits or earnings - they don’t mean what you think they mean. A loss making company is bad right? Well no, not if the losses are driven by R&D which is creating the basis for a really valuable cash-flow stream with little or no cash investment required and huge RoI. But of course a company that sells a dollar for 99 cents isn’t worth much.

A new paper from one of my favourite investment researchers, Michael Mauboussin draws this out really clearly.

the bottom line: there’s good losses and bad losses and you definitely need to know the difference as the “good losses” firms have vastly outperformed these last two decades.

Michael was on our podcast a few weeks ago (web | apple)!

3. On busy fools in investment research or why so much time & effort gets spent forecasting the wrong things (hello non-farm payrolls and next year’s earnings … ). By Joachim Clement.

I am slightly torn on this - agree for any investor forecasting next year earnings has little relation to returns. But someone needs to do it as having a consensus is valuable. Also in a competitive sales-oriented & noisy industry I don’t discount the value of forecasts in getting attention.

2 things I'm listening to

Expected Returns: Anti Ilmanen with Barry Ritholtz (web | apple). One thing that investors certainly should spend more time and effort thinking about are long term exepcted returns. These do matter.

Few folks have spent as much time on this as Anti Ilmanen and he walks us through how investors should start thinking about this most important parameter. Do current valuations matter more than long term history? Do risk-free yields matter? What about the oft-cited illiquidity premium. And don’t confuse GDP growth with equity returns (they aren’t linked).

Key insight: Investors who have commitments for the future (like defined benefit pensions) are more acutely affected by lower expected returns than investors who can just change their own expectations of outcomes.

2. Pre mortems: “Securities” with Danny Kahneman and Annie Duke (web | apple)

This is one of several brilliant short segments on risk and decision making with all all star cast of some of the best speakers imaginable on decision making including Danny Kahneman.

Pre-mortems. Why they help: Failure comes from a failure to understand failure. The framing effect of a pre-mortem encourages more and better thinking on risk. Pessimists are unpopular especially when a group is converging to a decision. But you need to permission it to happen.

Pre mortem doesn’t usually lead to decision change. What it does do is allow you to identify and close loopholes. Not a method for making decisions, but reducing strategic surprise.

Bonus froth

So it looks like the Amazon of heath care is going to be … Amazon. Just finished the Palace Papers, loved it - ties with the Bond King for my top summer reading rec.

And the most underappreciated thing in investing is …

So we wrapped up the podcast for the summer, took a little look back and whistle stop tout of the last 42 weeks since that “back to school” buzz we all had last September and the anticipation of a new world of hybrid working.

we also wrote down every single recommendation our guests have given us for books and podcasts!

Stay cool folks, enjoy the game ⚽️