La Rentreé

La Rentreé

Sentiment swings, inflation, key votes, long-term institutions, decision making and cringe

Some say the French concept of La Rentreé is far more than just “back to school”. Capturing the deeper spirit and atmosphere of renewal, page-turning and celebreation of this time of year (perhaps closer to new year’s than just back to school). I’m here for it!

Well hello there …

Aaaaaaand, just like that it’s September. Hope you had a great summer whatever you were up to. I spent a lot of time jumping into French rivers with an energetic ~2 year old, which was quite lovely. The rivers were unseasonably warm, great for jumping into but not so great for France’s legendary nuclear reactors, or more widely for water-bourne freight across the continent as water levels hit multi-century lows.

Catch up quick: markets.

We’ve had glass-half-full and glass-half-empty type sentiment dynamics over the summer, have you missed much? Maybe not - markets are at similar levels to where we were at the end of June.

The dip in US inflation announced in August prompted a stock market rise through to the middle of August (maybe the worst was over?), but stern words from Jerome Powell at the Jackson Hole confab (“we’ll do what it takes, even if it causes a recession”) caused that to reverse.

Bottom line: Markets care a lot about the Fed. We're in a strange moment for economic data. Good is bad (a booming economy means the Federal Reserve will tighten the screws more). And maybe bad is bad (nobody wants a recession).

Inflation is still the big, big news (but you knew that already). And of course, there’s an energy crisis which is only starting and looking so huge in scale in Europe it’s almost hard to grapple with. More on this in later newsletters but the Resolution Foundation in a briefing note have said that inflation looks set to wipe out twenty years of income growth in the UK, and could plunge 3 million more people into poverty. Grim stuff. Our new prime minister faces the immediate prospect of two lost decades.

Inflation in the world’s largest economies:

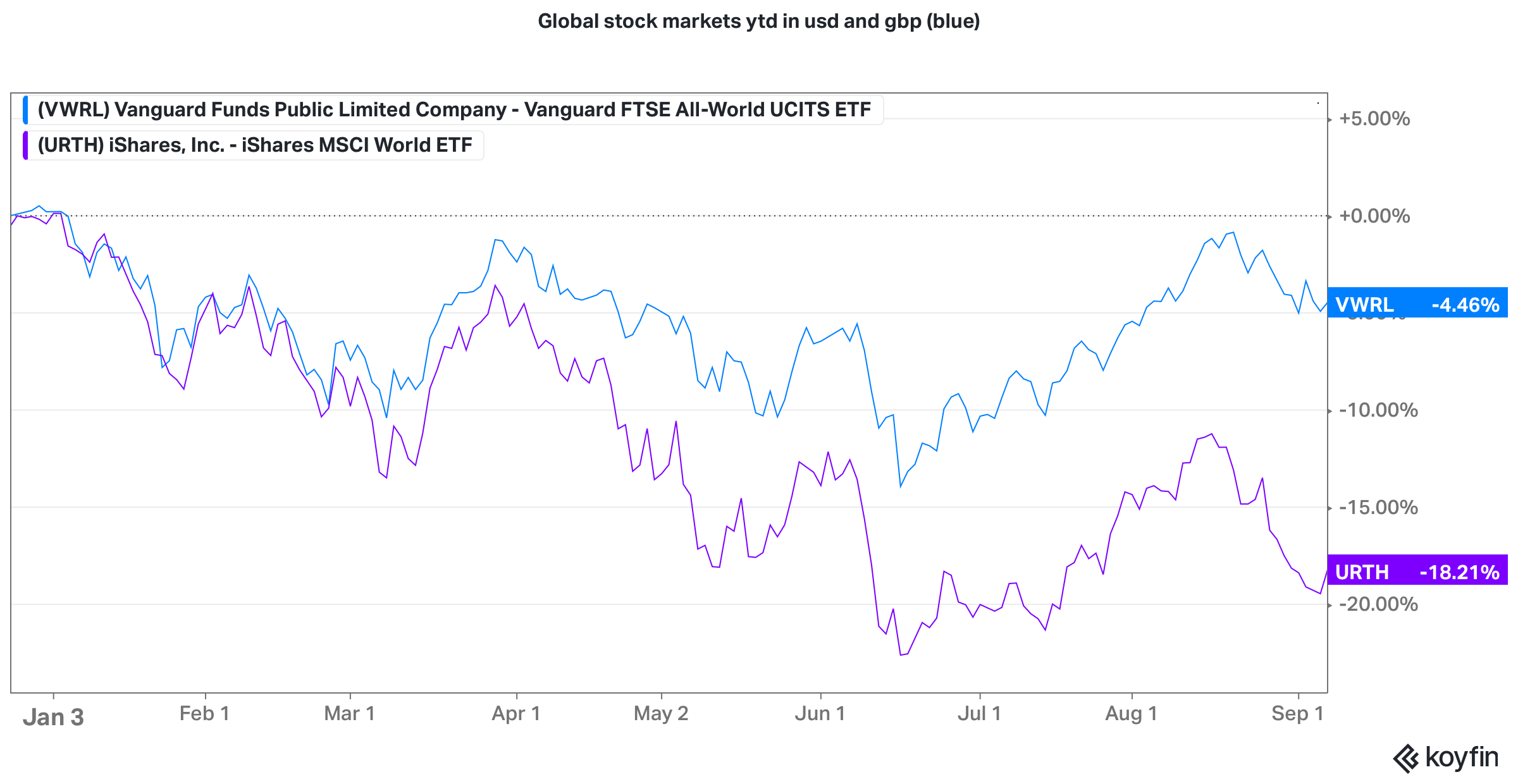

But also … sterling is falling- mind the gap between dollar returns and sterling returns. This really matters for sterling investors: global stocks in dollars are down almost 20% this year whereas in sterling the same portfolio is off just ~5%.

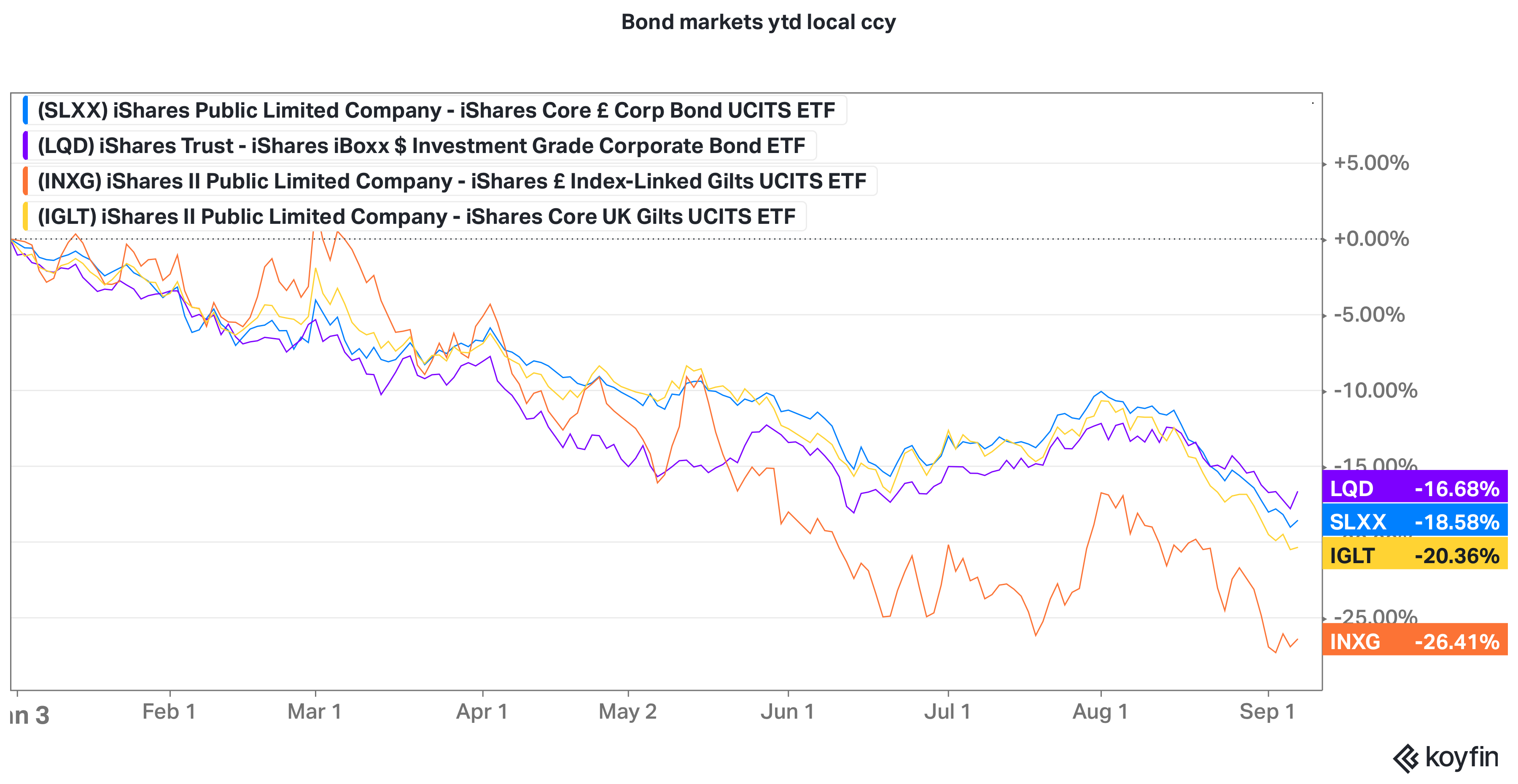

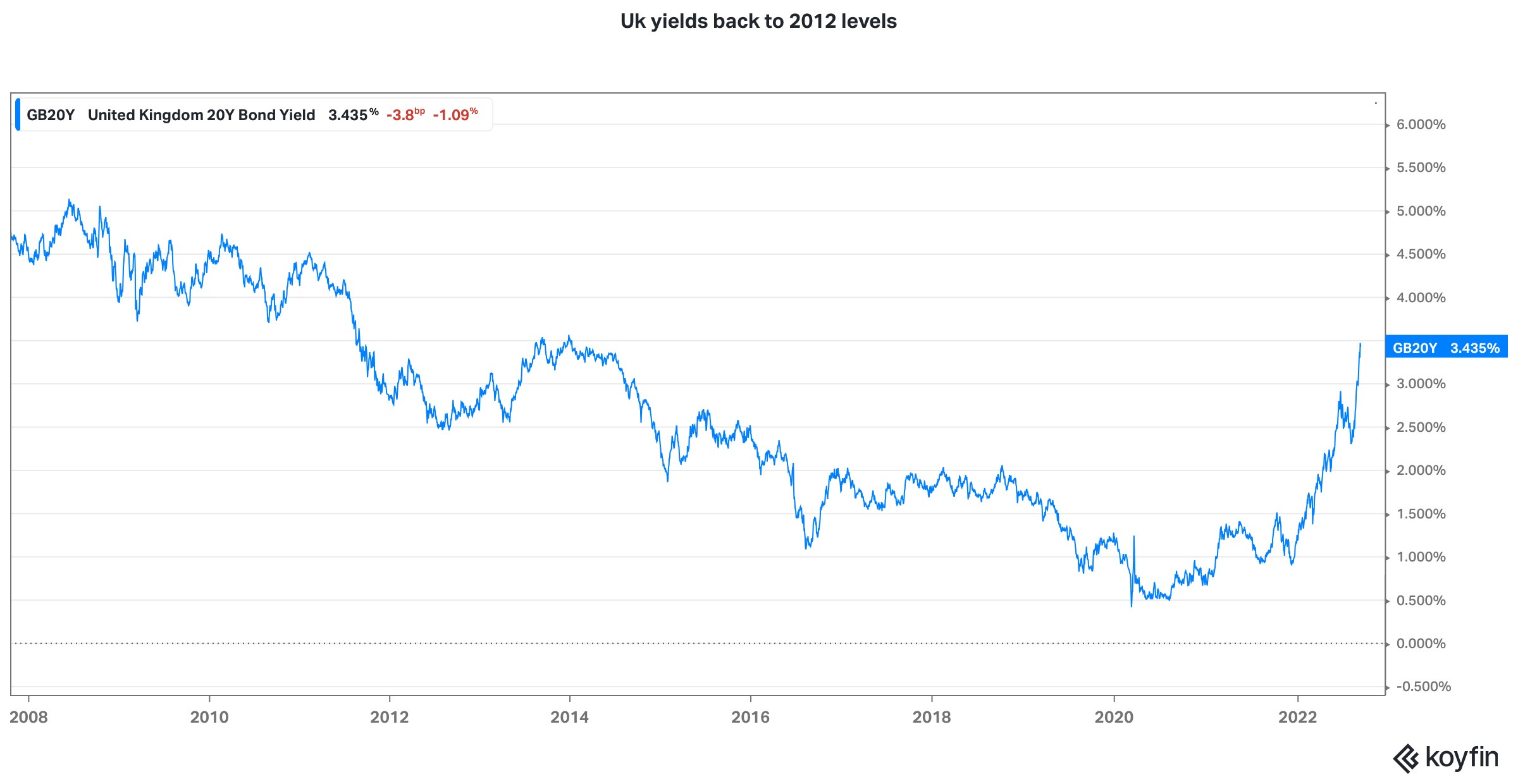

Bonds are back at the lows as interest rates have shot higher , again . Long-dated interest rates are pushing their highest levels for a decade in both the UK and US. Collateral top-up calls from LDI portfolios are coming thick and fast.

Yes but, lower bond prices means better yields and 96% of sterling corporate bonds now yield a healthy 4%, compared to just a smattering at the start of the year.

My view: price drives narrative a lot of the time not the other way round. The outlook is incredibly foggy and the truth is no-one really knows what’s going to happen - pays to remember this.

Three things I’m reading:

The JP Morgan guide to the markets (link) is just out updated to the end of august and is always well worth a look. My quicktake on the economic and markets story contained therein is:

Company earnings are strong and

The US labour market remains very strong but

Inflation is off the charts almost everywhere so

Central banks are still, still, raising rates and surprising markets all over the place but

Markets think inflation calms down soonish but interest rates are the real story which means

Stock and bond markets are down, price-earnings valuations are back to average levels and

Credit market spreads and yields show some of the best opportunities in a decade

WFH. Speaking of Rentreé, a year after the big return to office phase of September 2021, where are we with WFH practices, here’s some interesting data:

50% of visits to the office were for only one day a week according to data from Basking.io, a workplace-occupancy analytics company (per Bloomberg)

Looks like we might be stabilising at 30% WFH overall says Nick Bloom, a huge labour market shakeup vs pre-covid.

Shareaction votes to watch - the results, what happened? (blog)

Of ShareAction‘s 20 votes to watch, none passed (takeaway: resolutions are hard)

Although 3 were withdrawn , suggesting some success in getting company to take action (takeaway: it’s not all about votes)

Climate still gets most support

But support on workers rights is growing (note resolution on workers rights at Amazon garnered most support at 39%, takeaway: asset owners need to take a view)

One common reason for asset managers not to support is a feeling a resolution is too prescriptive on management .

But if they are just enforcing a commonly agreed standard then how controversial are they really? Takeaway: asset owners need to try and understand

final takeaway: votes matter, and asset owners are going to be spending a lot more time looking at this.

Two things I’m listening to.

The Long Now seminars (web | apple). I’m fascinated by this idea that universities are among the world’s longest lived institutions because they are required to reinvent themselves every year for a new cohort of students

four stages of expertise :

1. Mental model of how things work

2. Understand edge cases & limitations

3. Know how to overcome limitations

4. Anticipate areas of common resistance

3 pathways to insight:

1. Connection: 2+2 = …

2. Contradiction + curiosity “that doesn’t make sense , why “

3. Resistance. This isn’t working. Why?

Yes, but: But: Companies & institutions tend to reject insight

Bcos it requires change & could be disruptive

“Knowledge shields” cause folks to reject insight

And new ideas are fragile: only usually needs one person among many to reject

In this week’s charts that make you go hmmmmmm:

One thing to brighten your day:

“Cringe is a core part of our voice here at LinkedIn”. Hilarious Dan Toomey imagines the linkedin CEO defending the platform -