Long rates rising 📈 🌦️🏉

Long rates rising 📈 🌦️🏉

Homeland economics, everyone knows everything, the maturity wall, bond myths and Sam Bankman-Fried

Bonjour October!

That lovely little warm snap has come to a sharp end today and those waterproofs and down layers look like they are getting good use on the morning commute. Before you know it it’ll be 2024 macro outlook season.

Big week in our household with a couple of birthdays for the little ones. What a joy toddler birthdays are! I do love a toddler party, despite all the chaos, although for me there’s still a lot of novelty to it so I may revisit this view after a dozen or so of them, we’ll see.

Be honest - do you own a pair of Birkenstocks? I caved over the summer and have to admit that Mrs M was right, they are a revelation in comfort. What is more surprising is the company is now stepping out into the global listed markets in what’s seen as a toe in the water for global risk appetite during a tentative re-opening of the IPO market. The stock was down a fair bit on the first day though, so buckle up.

]It’s been such a terribly dark week in global news hasn’t it, there’s no getting round it. But lets talk markets because that’s what you’re here for -

Markets mumble

A soft landing is possible in practice, but is it possible in theory?

Stocks are about the same level as they were two weeks ago - your global stocks are up about 13% for the year (and 30%+ over three years), without the US it’s more like 5-8% this year. But the big story is in rates …

That the market has finally come round strongly to a narrative of higher for longer interest rates perhaps shouldn’t be so much of a surprise. But exactly why that happened so abruptly and fast in the last few weeks is harder to explain, but of course it doesn’t all have to make sense. The global surge higher in long dated rates began with the release of the dot-plot 3 weeks ago, but continued pretty relentlessly and even getting a boost from a very strong jobs report last week in the US, although yields did fall back quite a lot on Monday of this week with some Fedspeak talking rates down and probably some safe-haven reaction to those awful attacks in Israel.

And of course the question is what does this rise in long-term rates mean for stocks, for interest rates for economies etc.

That yield curve inversion that we’ve had for many months now is evaporating faster than you can say positive term premia. Does it matter? It’s usually a good signal of recession, we’re told. But maybe this time it is different. The financial sector sure has less of an influence on the economy these days and that’s the most direct tangible transmission of the inverted curve. Maybe the bond market has just got really bad at forecasting rates, or maybe the bigger problem is it just constantly changes its mind.

Things I'm reading

The Economist led last week on homeland economics - are free markets history? (link)

Now you’ve got to take into account the fact the economist is well known for being a contra-indicator on some of these big trends: by the time they’ve written it up it’s probably time to bet the other way. But there’s surely a good few conference panel sessions left in this particular theme and what it means for investors. More home bias? Different thinking in emerging markets? Currency hedging?

Keeping it simple in investing by Jan Loeys [link to FT article]

The bottom line

How many assets do you really need in your long-term portfolio? Two (a global stock fund and local bond fund)

Are there any superior assets left that you should systematically overweight in a strategic portfolio? Not any more, everyone knows everything

I love to see it. I think complexity gets put on a pedestal far too often and this creates real problems because it becomes the expectation. But you can see why, complexity superficially signals effort and expertise and cleverness. It feels like real work, while simplicity can look naive or, well, simplistic.

And there are tangible advantages to simplicity: you can far more easily stay on top of performance and what’s driving it, and you’re less likely to constantly tinker and add/subtract strategies and managers.

It’s easy to say but real work to internalise it and actually live by it I think.

It’s time to vanquish those bond market myths says Allison Schrager (link)

they aren’t risk free (hello, duration)

central banks don’t drive rates (hello term premium, inflation premium - things we realistically know very very little about)

demographics won’t drive rates down by destiny (hello supply and demand)

I’d pitch to add bond / stock correlation to this and the idea of bonds as a risk-off hedge.

The big picture

We need to spend more time vanquishing market myths! There are few immutable laws in investing but stable features of an environment get quickly built into how things work and aren’t challenged enough.

Specifically for allocators there’s questions about bonds here. When you do and don’t want duration, and how to calibrate long term expectations of term and inflation premium to size your holdings, among other challenges. Astute readers might recognise these as key questions for a large DC Mastertrust running fixed income as a diversifier alongside growth assets, as an income generator in drawdown and as a risk-reducer for folks heading to cashout.

Howard Marks also has thoughts on asset owners allocating to credit in his latest memo (tl;dr do more of it) (link)

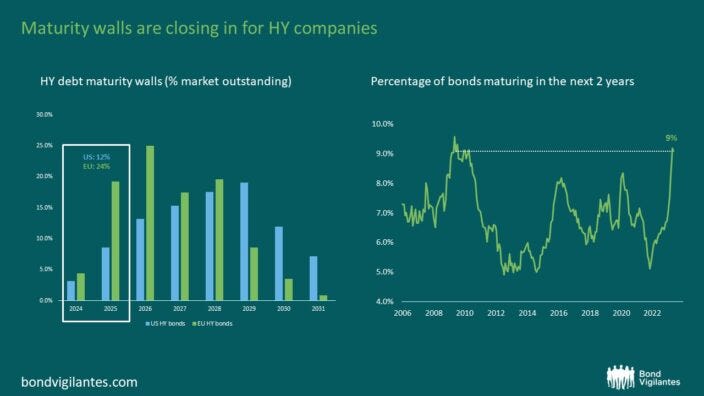

Ana Gil at Bond Vigilantes previews the potential High Yield maturity wall (but why it’s not as bad as you may think) [link]

High yield spreads have been a bit weird the last few months, driven tighter by a very light issuance calendar in the face of higher rates, but doesn’t that have to change at some point? Yes, says Ana - look out over the next two years

Duncan Lamont reminds us that outside the top-7 stocks, markets are probably much cheaper than you think (link)

Come for the narrow market, stay for the opportunities. It highlights the nub of the issue for many an active manager, if you haven’t owned that small group of stocks your performance is looking pretty ugly, but the opportunities around look great.

But the second dilemma is that tonnes of opportunities might exist but with less catalysts to return them to “fair” value over a sensible timeframe (due to less active managers existing) you might well make outperforming harder not easier.

Things I’m listening to

Lewis is out with a new book, on FTX and Sam Bankman-Fried (“Going Infinite”). Important background! There’s a knock on Lewis here in that he got too close to his subject and now finds himself excusing one of the most egregious frauds in history. In his defence Lewis says he wants to paint the picture and let the reader make up their mind.

Weirdly, as they discuss in the conversation it looks like FTX customers may recover almost 100% of the funds they had on the platform, as the assets of FTX (including a portfolio of VC stakes, including anthropic, an AI firm) may come up to the total liabilities.

Anyway, this is definitely worth a listen, and I’ll probably be getting the book too.

Don’t call it a soft landing, it’s a golden path now says Austan. It’s an enjoyable run through of where we’re at in bond and rates markets.

Rory Sutherland with Lex Friedman

I only managed to make it through most of this 3 hour epic conversation thanks to a couple of long solo car journeys to the last Spartan race of the season, but it’s a wonderful meander through the mind of Rory Sutherland which is quite an interesting place. Gems:

The opposite of a good idea is usually another good idea

Split your focus between the specific and the speculative (some bees don’t do the waggle dance)

A logical decision comes with built in rationale but often adds little value as “everyone knows everything”

Mandevillian intelligence: lots of people being stupid in different ways aggregates to something intelligent

Grab bag

Things are so weird in the bond markets it may be that you lost more money on the Austrian 100-year bond than the defaulted Argentinian one says Robin Wigglesworth.

With rugby a huge source of conversation at the moment I did enjoy the Danny Cipriani autobiography, if you’re a big rugby fan and an England follower.

Thoughts for this weekend’s quarter finals? Some amazing match ups. I’m tempted to go for an all northern hemisphere semi-final line up coming through.

Have you started the Beckham documentary yet? Of course you have! What’s not to like about a bit of 90’s UK nostalgia

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser