Melt-up 🔥📈 🚀

Melt-up 🔥📈 🚀

Inflation, stocks soar, a crypto crisis, easy data bias and stakeholder capitalism

Hi there 👋 welcome back. So who plays Sam Bankman-Fried in the movie? Jonah Hill seems a dead cert for that, no? More on crypto later.

How’s November looking for you? Gotta say, it isn’t a month that blessed with natural highlights, is it. Been raining ones and zeros here for what seems like a year. Coffee is still served strong here though - grab a cup and let’s dive in.

I tell you what bath/bedtime with a toddler plus newborn is a bit like those double stacking F1 pit stops, but more chaotic, drawn out and involving more shouting and tears … Box! Box!

Right, markers stuff 👇

Is it a head fake or is it the real thing? Who knows, but markets loved the slightly-lower-than-expected US inflation numbers last week spurring stocks to surge faster than crowds at a Harry Styles gig (so I’m told, anyway). Soft landing is back on the table.

5% up days are pretty rare! They’ve usually happened during bear markets not surprisingly, when pessimism is high and expectations low which drives things as much as the actual news.

The big picture: It really is still just guessing games on every single datapoint right now as we’re at such a sensitive inflection point, everything has more meaning than it probably should. To help make sense of all this I’d recommend our recent conversation with JP Morgan Chief Strategist Karen Ward (here) - assessing where we’re at in the rate hiking cycle and what matters from here. Talking to Karen helped me get me own thinking clearer on what matters.

Q: even if you knew the inflation number would you have guessed the market reaction? Like, maybe … but not really? Calling turning points is super hard, and every narrative seems to make sense when you hear it.

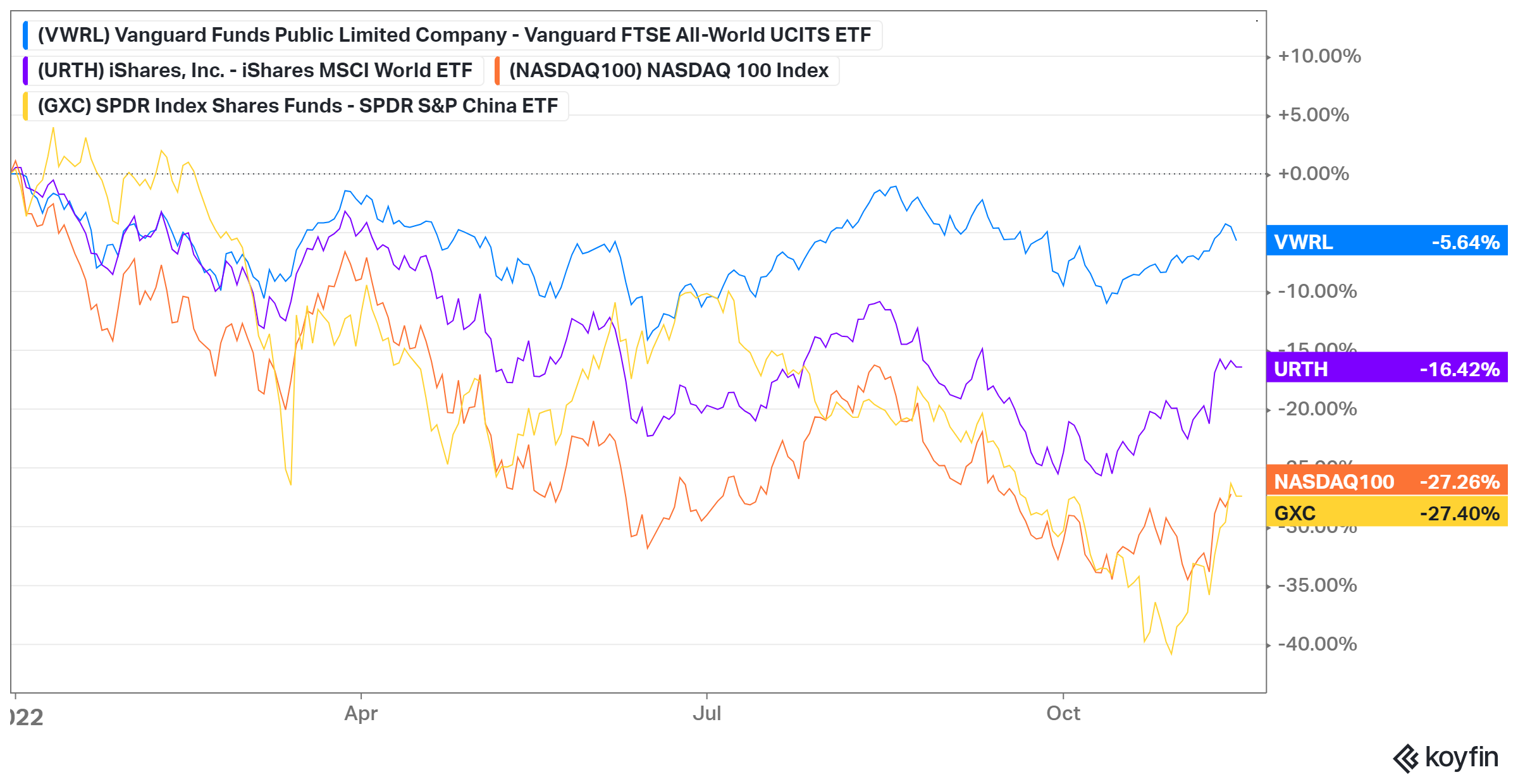

Charts: global stocks in GBP now back within shouting distance of flat for the year. Some of that China stuff has really bounced since last time too.

And long-dated rates are a little back from the highs

Ok, so, let’s do the crypto stuff. This was kinda last week’s news so I’ll spare you the play-by-play you’ve already seen ten times (highly recommend Matt Levine for that whose stuff is also very humorous), the two key points for me: customer funds go missing to prop up failing trading arm (ahem, hello MF Global) plus crypto magic-money box thing wherein you issue a token, manipulate the price up on small volume and then make that look like real assets on a balance sheet against real liabilities. And that’s key: it’s all fun and games when dog-meme-coin-price-go-down but when the magic stuff is supporting borrowing or supporting “real” liabilities (like, erm, the need to pay back folks who placed their assets with your exchange) then you have a serious problem like at FTX.

Some takeaways:

When the winter becomes an ice age…

I agree with Joe Weisenthal that this hits different to all the other negative crypto stuff over the last year - it’s far far worse. I’ve tried to stay open minded on the space as it came up with new questions to ask about old problems (if not actual solutions) and had a different way of looking at the world which even when it was wrong, was maybe wrong in useful ways.

But this could be the end of real institutional interest in the space. Sure, there’s still a surprisingly large amount of wealth that “wants” to be in crypto, and that’s fine. But the bull case was based on mainstream adoption and maybe new interest has just totally peaked out and the reason is trust: FTX was blue-chip by crytpo standards. It was supposedly a real thing, it was bailing out other crypto stuff. Real people had invested real money.

Your knee-jerk haters and die-hard maximalists will always be shouting past each other but at some point the narrative of your average open-minded person has to tip from "the bear market in crypto is weeding out all the froth" to "it really is just scams and sh!tcoins all the way down." Having nowhere safe to hold your assets other than in the mattress means the industry is uninvestible at scale.

has a good piece, his take: what if crypto just, dies?Things I’m reading

- probably has the best helicopter view on this crypto stuff in her piece on trust. (Link)

A thing that matters: Halo-effect is really real and it can be manufactured. FTX founder Sam Bankman-Fried was pictured onstage chatting with Bill Clinton and Tony Blair. Tom Brady was a promoter, FTX was on sports stadiums for goodness sakes (I think there’s another whole piece to be written on the dangers of the soft-power and unearned legitimacy that can be gained through sport, hello FIFA, hello F1). We need to recognise that unearned credibility and social proof are a thing, and manipulate us in ways we can’t even begin to imagine.

HE RAISED $2bn AND DIDN’T EVEN HAVE A BOARD!

Ben Carlson says in investing, boring is in fact beautiful (link)

In short: French philosopher Blaise Pascal once wrote, “All of humanity’s problems stem from man’s inability to sit quietly in a room alone.”

The investor play on words here would be: “All portfolio problems stem from investor’s inability to stick with a boring old asset allocation.”

Institutional folks will tut-tut away at all the memestock and profit-less tech speculation among individual investors but they ought to look at themselves a bit as they can have their own “shiny things” in the portfolio too.

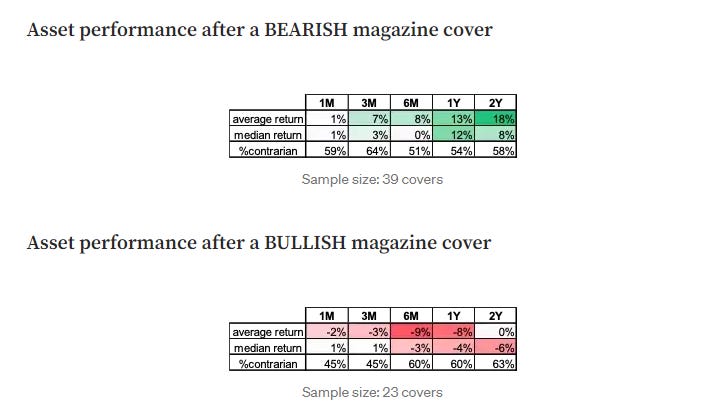

The Magazine Cover Indicator - it’s a real thing! (Link) Brent Donnelly has crunched some numbers…

It’s especially relevant after all the fun that’s been had laughing at the OTT magazine profiles of SBF.

The bottom line: DO THE OPPOSITE. As we all may have secretly suspected, Economist covers are empirically a contra-indicator, particularly in commodities. Doing the opposite of the cover story is a positive value strategy.

It makes some sense: in a world of cycles, by the time a theme has been around long enough for editors to commissions journalists to research and write long pieces on it maybe the cycle has turned before that piece sees the light of day…

I know what you’re thinking, here’s what’s been on recent covers (UK version). The conclusion would be to get extremely bullish on the UK right now!

Two things I’m listening to

Rational Reminder: Scott Cederburg on long run losses in stocks and bonds ( web | apple)

Great little insight from this that I think we’re all guilty of a bit: easy data bias. We use the data that fits our analysis structure (monthly, certain dates etc). And this itself creates an upward bias in all research which is easily ignored (hello S&P 500 since 1970, easiest stock market data to grab and work with, also the best performing market). It’s sort of a close cousin of survivorship bias wherein we’re always working with data that is upward biased, because the bad stuff is messy has bits missing where there were revolutions etc.

All Else Equal podcast with Alex Edmans on stakeholder capitalism (web|apple)

Cracking little energetic debate on shareholder and stakeholder capitalism, externalities, regulation, etc with a lively exchange of views and perspectives. Just listening to the first ten minutes is an excellent exploration of some of basic viewpoint here and the counter arguments.

Bottom line: stakeholder capitalism isn’t about being all things to all people, it ought to be something where the company has a competitive advantage and stakeholders can be well defined. A mandate from the shareholders (eg Say on climate votes) is important . It is not as different from a strict shareholder focus as you first think - many stakeholder issues DO boost profits in long run (it’s just hard to demonstrate it on a spreadsheet). And government regulation isn’t the panacea you might think - it has it’s own difficulties with practicalities and there are things that governments can’t or won’t regulate or tax.

Grab bag

As the LDI committee appearances begin, Toby Nangle did some polls. I think the one where votes are split evenly is quite interesting. It’s really not as easy as most folks like to think to parse the real causes. Sure everyone jumps to the conclusion implied by their prior beefs, but to learn the right lessons you need to get the causes right.

Do take a little look over at our investment magazine Vista - I’ve got a piece in there sharing thoughts on shareholder voting, why we saw less support for ESG-related votes in 2022 and whether this matters.

Anyone got into the crown yet? That’s next up. Popcorn time. Also heard the wirecard netflix thing is worth a watch.

I had the great fortune to see Mo Gawdat speak recently. He’s got some great things to say about living in the moment and that little voice in your head. Here’s one of his videos to put a little positivity into your week:.

Have a great rest of week! anyone had a mince pie yet?! I promise less crypto stuff next time …