Selling in May

Selling in May

Things you see in every bear market, beliefs, better questions proxy battles and “good enough” as the new perfect

Yikes. Are we at the “Warren Buffet quotes” or the “Mike Tyson quotes” stage in this bear market? Every. Single. Time. You always hear the same stuff in every bear market (Ben Carlson writes): every strategist trying to make a name for themselves, lots of “cautiously optimistic”, the perma-bears coming out to play and “death of diversification” headlines.

Unless you’ve been living under a rock you’ll be aware that these are not good times in the stock market. But what to call it? An orderly decline? Correction? Valuation reset? I think the offical bear market committee have taken a look at the intraday data and voted marginally that the broad market doesn’t quite qualify (last I heard) - yet.

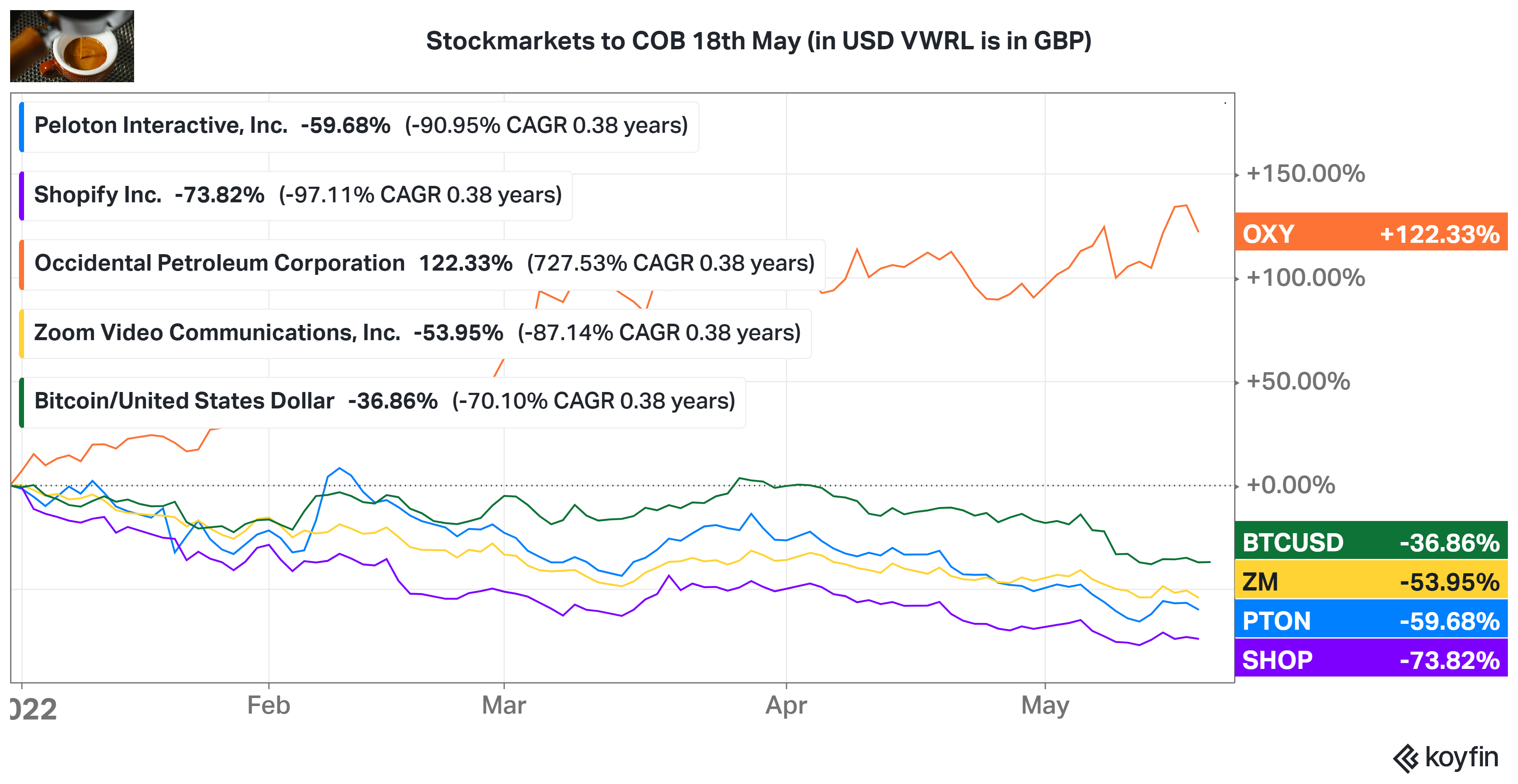

Tech stuff is another story - you want to know how much you’d now have if you invested £10,000 in Peloton a year ago? Not enough to buy one of their stationary bikes. Now do Zoom. Coinbase.

The only bull market right now is in commentary. Oh, and style premia and trend funds are crushing it year to date. Where are we on Value/Growth? Cliff Asness says: still crazy.

At times like this the risk is spouting too much mumble but saying nothing useful, or not saying anything at all. I’m going to try for a middle way. In downmarkets a lot of the same things bear repeating: better future returns, more reasonable valuations, this is all normal, don’t forget your equities have still almost doubled in 5 years (covered a lot of this last time).

If you think markets are hard to predict now, don’t forget that’s always the case. A lot of the commonly cited indicators are nowhere near as powerful as you think.

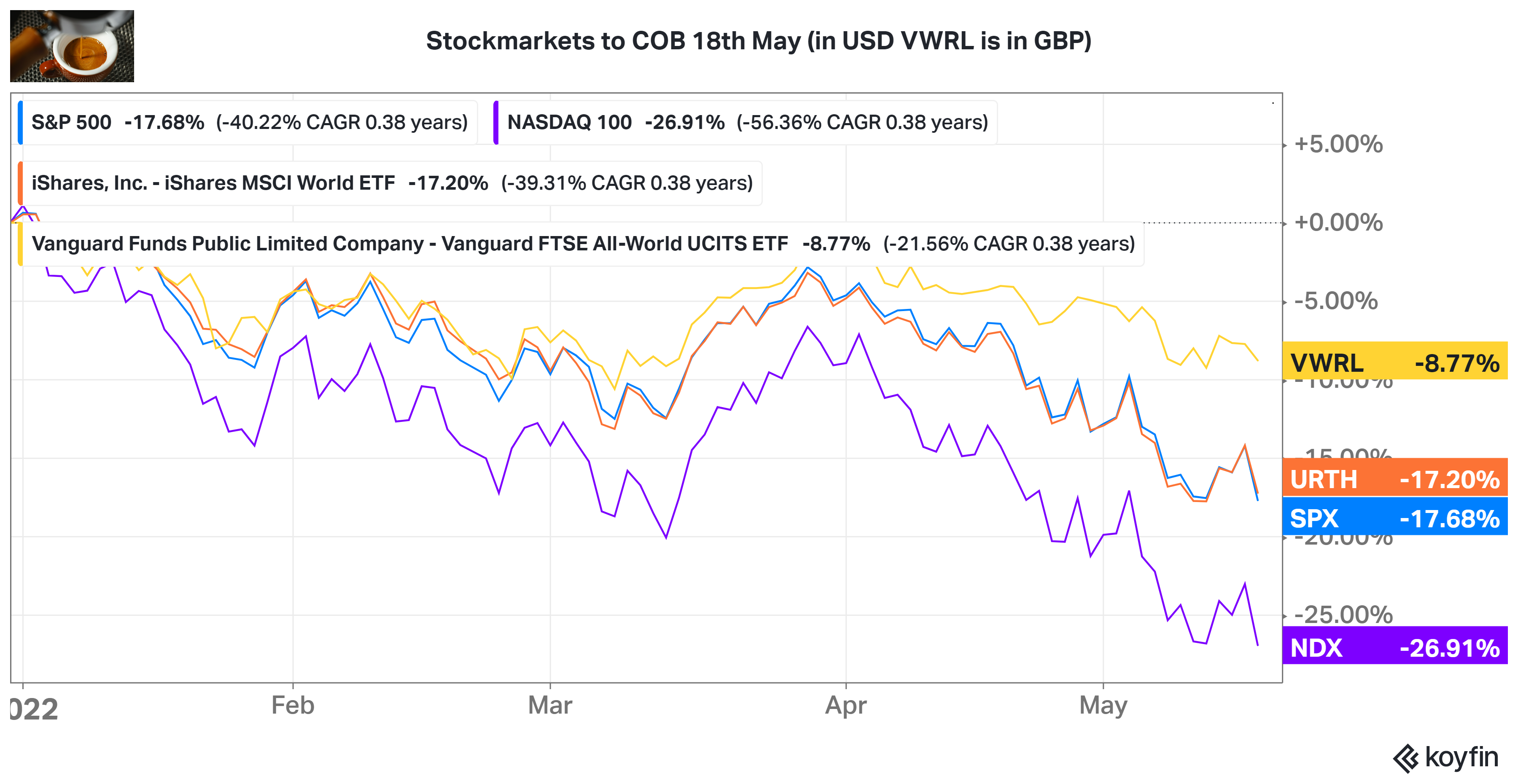

Here’s stock markets - things have slumped a fair bit in the last two weeks - incuding a big 4% down day yesterday (wednesday). For an unhedged sterling investor the currency has still taken a lot of the edge off the falls though (yellow line tracks a global equity ETF in sterling whereas orange line is a similar thing in USD).

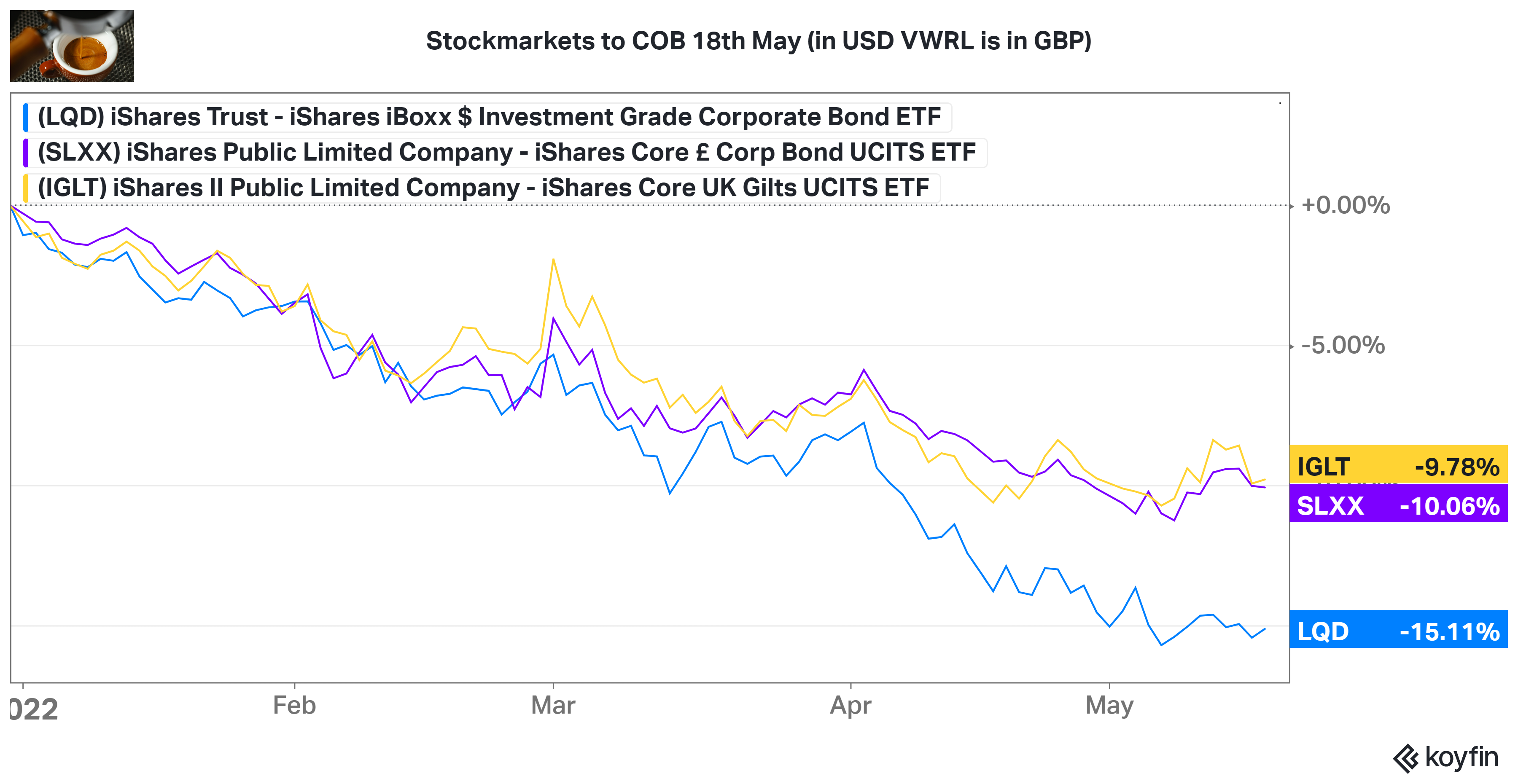

Bonds - still in a hole ytd, not much change there. It remains one of the biggest bond bear markets ever (certainly in $ terms). Investors are getting a second bite at the cherry with high grade corporate bond spreads back up to good levels around 1.5%. All-in yields are at decade highs in high grade.

Some of the individual stock charts are pretty wild -

But also …

Economic/earnings updates: there’s been a batch of pretty positive economic data in the US as well as corporate earnings that beat expectations by c12% and future earnings expectations revised up [per Ed Yardeni] seems like a battle between bullish analysts, bearish investors and bullish consumers.

The Fed is hiking like it’s ‘99, but said they wouldn’t raise by 75, but actually like, maybe they will? 🤷♂️

Recession of course is the big worry - are markets pricing it already? See podcast rec’s for a discussion of whether this could actually be the weirdest recession ever. Could things actually be going “pretty much according to plan” (tighter financial conditions, less froth) asks Kristina Hooper [blog]

Inflation charts are going vertical. The only positive is maybe it has peaked?

Sound smart by saying: is the Fed put getting re-struck downward here?

Aswath Damdaran has written one of the better takes stepping back and thinking through where we are now from a macro perspective and setting out 4 ways things could play out.

The nature of markets is that they are never quite settled, as investors recalibrate expectations constantly and reset prices. In most time periods, those recalibrations and resets tend to be small and in both directions, resulting in the ups and downs that pass for normal volatility. Clearly, we are not in one of those time periods, as markets approach bipolar territory, with big moves up and down.

to understand inflation's impact on asset values, you have to break it down into its expected and unexpected components, with the former showing up in the expected returns you demand on investments, and the latter playing out as a risk factor

Three things I’m reading

1. Morgan Housel is writing about a few beliefs, every word of this is gold

http://www.collaborativefund.com/blog/a-few-beliefs/

A lot of denial masquerades as patience.

A lot of people have a hard time distinguishing between what happened and what they think should have happened given their world view.

Having your views confirmed is a powerful and addictive drug.

Many bad investment decisions are good ideas taken too far.

Unsustainable things can last years or decades longer than people think.

Tell people what they want to hear and you can be wrong indefinitely without penalty.

2. I think Asking better questions is an absolute art and an underrated one at that. Tijs Besieux writing in HBR has set out three properties of a good question [article]:

It shows you have prepared

It showcases, but doesn’t show off, your expertise

It invites the other side to deepen or broaden their thinking or question a key belief

I think the last of these is maybe the most important.

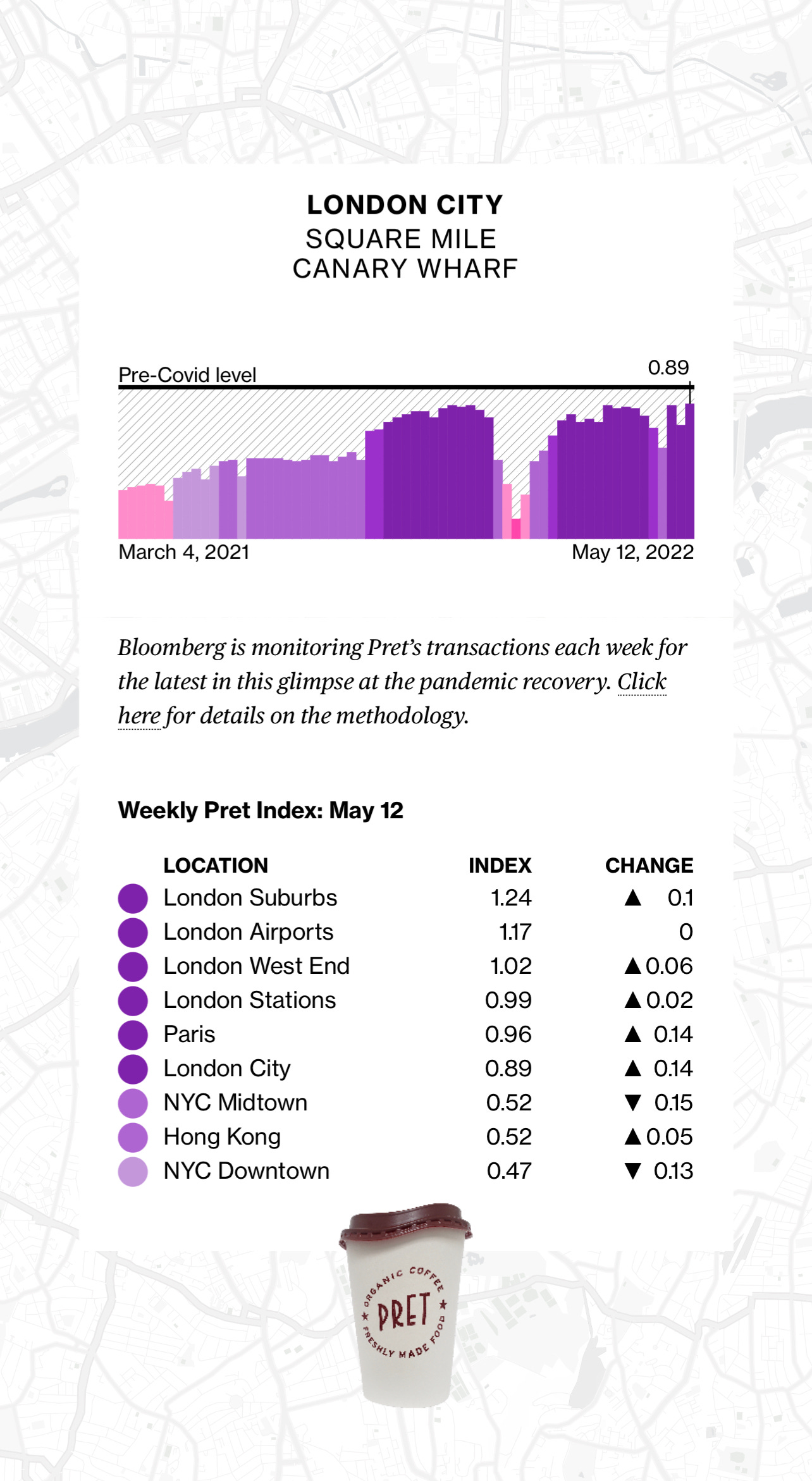

3. In person is back. I mean back, back. And we have the data to prove it. One indicator that is hitting new highs is the Pret footfall index. which anyone who has been into central London recently on a sunny Thursday will immediately understand. London airports and suburbs have surged to new highs, the West End is up above pre-covid and the city is only 10% off. New York seems the big standout only around 50% and falling. I’ve been out and about a fair bit this month and it’s been so rewarding to meet many of the readers of this newsletter in person, I really do appreciate it!

2 things I’m listening to

The Economist Money Talks on proxy voting (web | apple). Proxy voting is big, and it matters. Frequently it’s the influence point of choice for investors looking to shift corporate practice on climate and other issues, and broader media is waking up to it. Some great inside persepctives here on resolutions at Berkshire Hathaway and others.

2. Derek Thompson asks Michael Batnick and Ben Carlson - Could this be the weirdest recession? (web | apple) The conundrum here is the idea of a possible recession while consumer and corporate balance sheets remain on average pretty strong, and unemployment is at all time lows. I guess things are always weirder than you think and this time is always different.

Bonus froth

is “Good enough” the new perfect asks Joy Lere

Moving your aim from "perfection" to "good enough" doesn't mean you settle, give up, or get a pass for hurtful behavior. Instead, the recalibration of internal expectations shifts how we respond to ourselves

I wrote a thing on greenwashing, it seemed to resonate.

One thing to brighten your day - Ryanair trolling the crypto bros is … *chef’s kiss* #welcomeaboard