Seventy-Five😎

Seventy-Five😎

Fed watching, defaults, the China question, divestment, why do investors really like illiquids + a bull market in doggie ice cream

☀️☀️Scorcher of a week here in London - hope you’re all getting out of your office caves for a bit folks! ☀️☀️

So it’s official - we’re at the Warren Buffett quotes stage of the bear market: “Buy when there’s blood in the streets even if you’ve been punched in the mouth … be greedy when the markets a voting machine unless it’s different this time”

Two huge episodes on the podcast these last two weeks. We had one of the foremost thinkers in responsible investing - Alex Edmans talking growing the pie (web | apple ), and we had Dr Rebecca Newton on all things work life: seasons, joy (yes really), intentionality and energy. Great stuff. Listen here (web | apple).

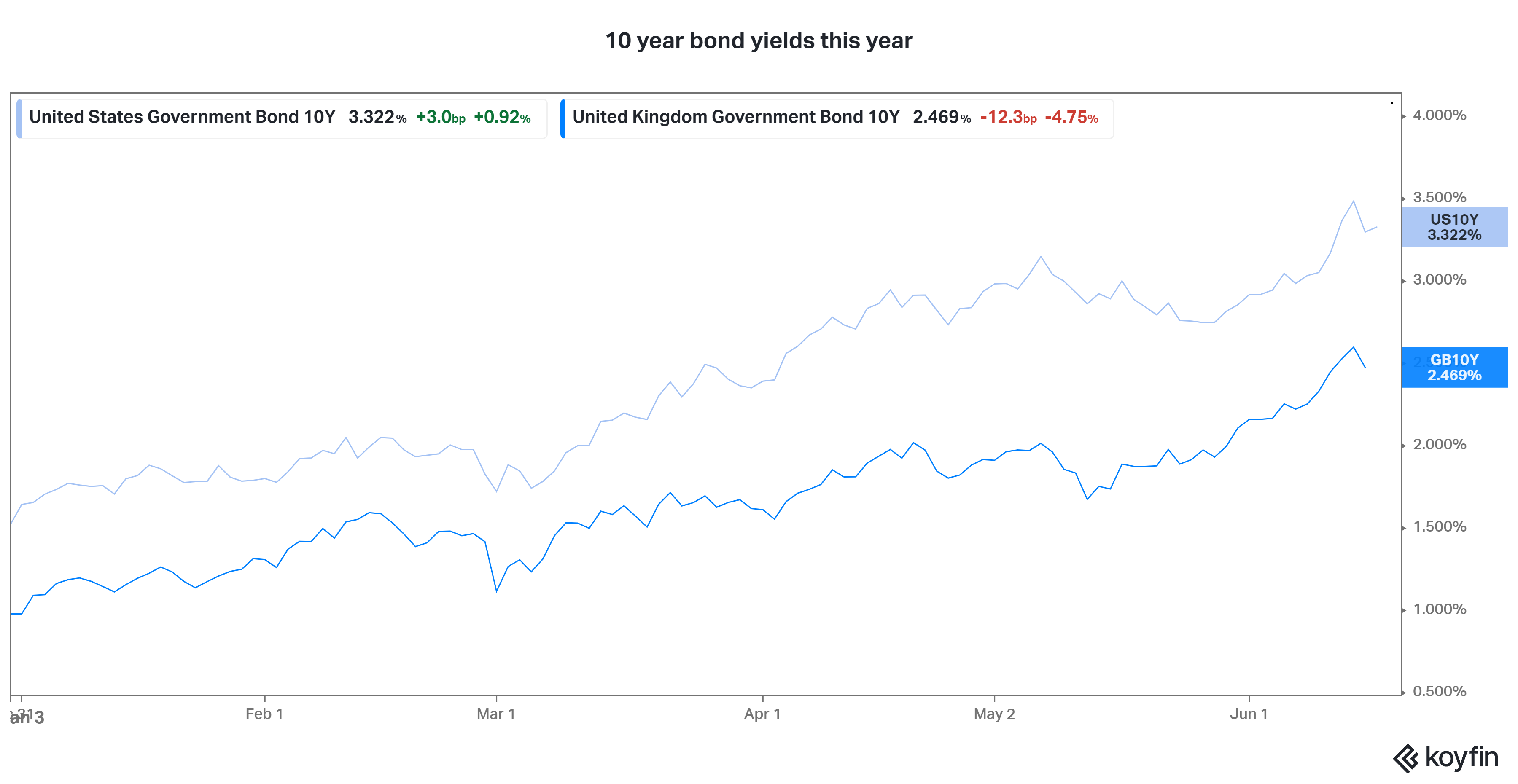

Well we all know it so I’ll just say it: the Fed is the only game in town in markets yet again. As wise heads say: “if it depends on the Fed decision, it’s not a long term investment”. Words to live by, and kudos to any long term investor who can genuinely shut out noise around the Fed at times like these. I will say though, I do think there’s something in these potentially quite pivotal Fed decisions here that raises them up above the base level of market astrology and into the realm of the long term investors trying to weigh the likely longer term level of risk free rates.

For a full Fed deep-dive I recommend John Authers column this morning: So Now We Have Clarity. The World Has Changed

Spoiler alert: inflation didn’t peak.

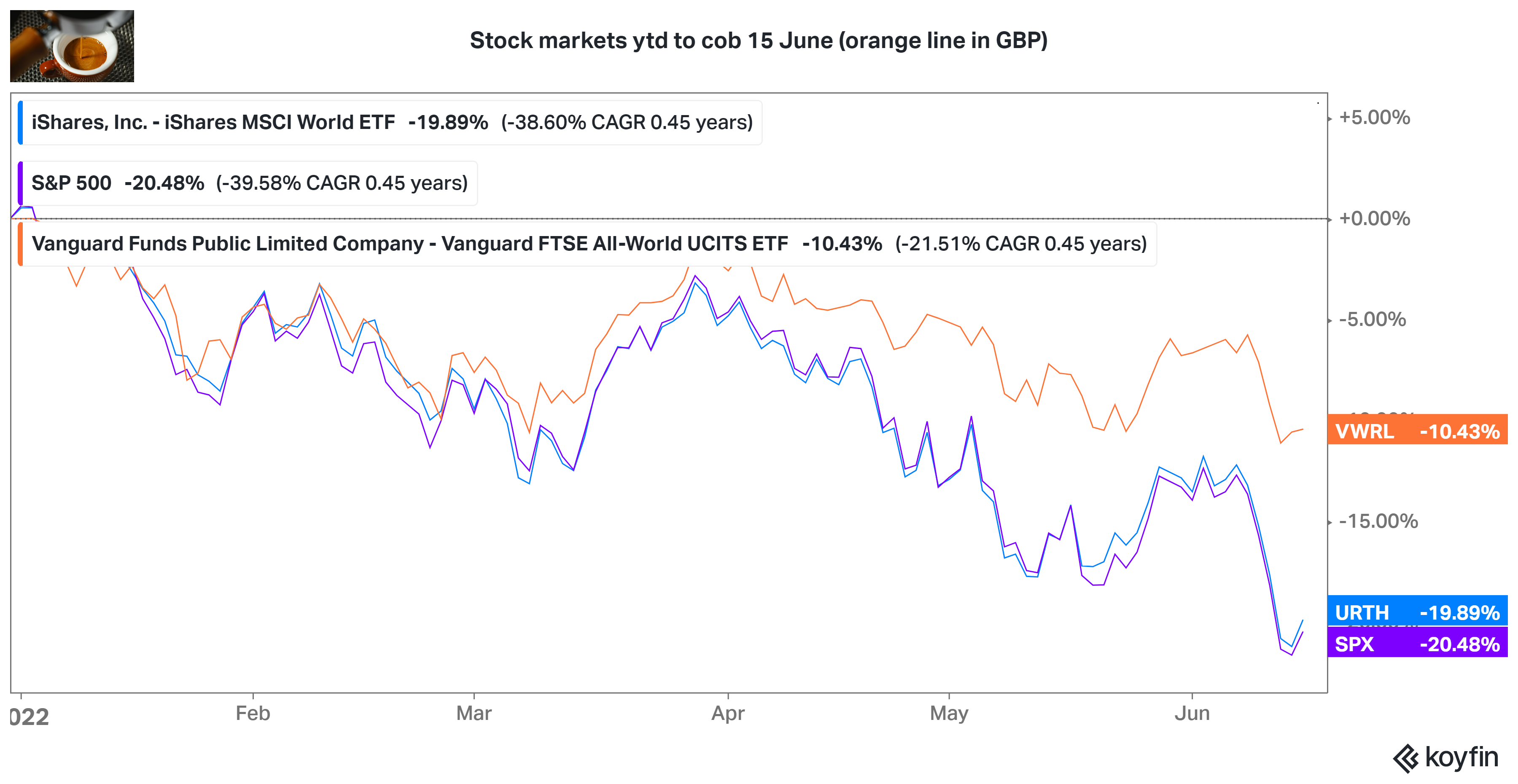

Right then - in stock markets: a new low and a bounce. How many times have we said that this year? Choppy. It’s the 13th bear market decline since WWII (Ben Carlson writes) . The only bull markets are in commodities, certain liquid alts funds, crypto memes and commentary.

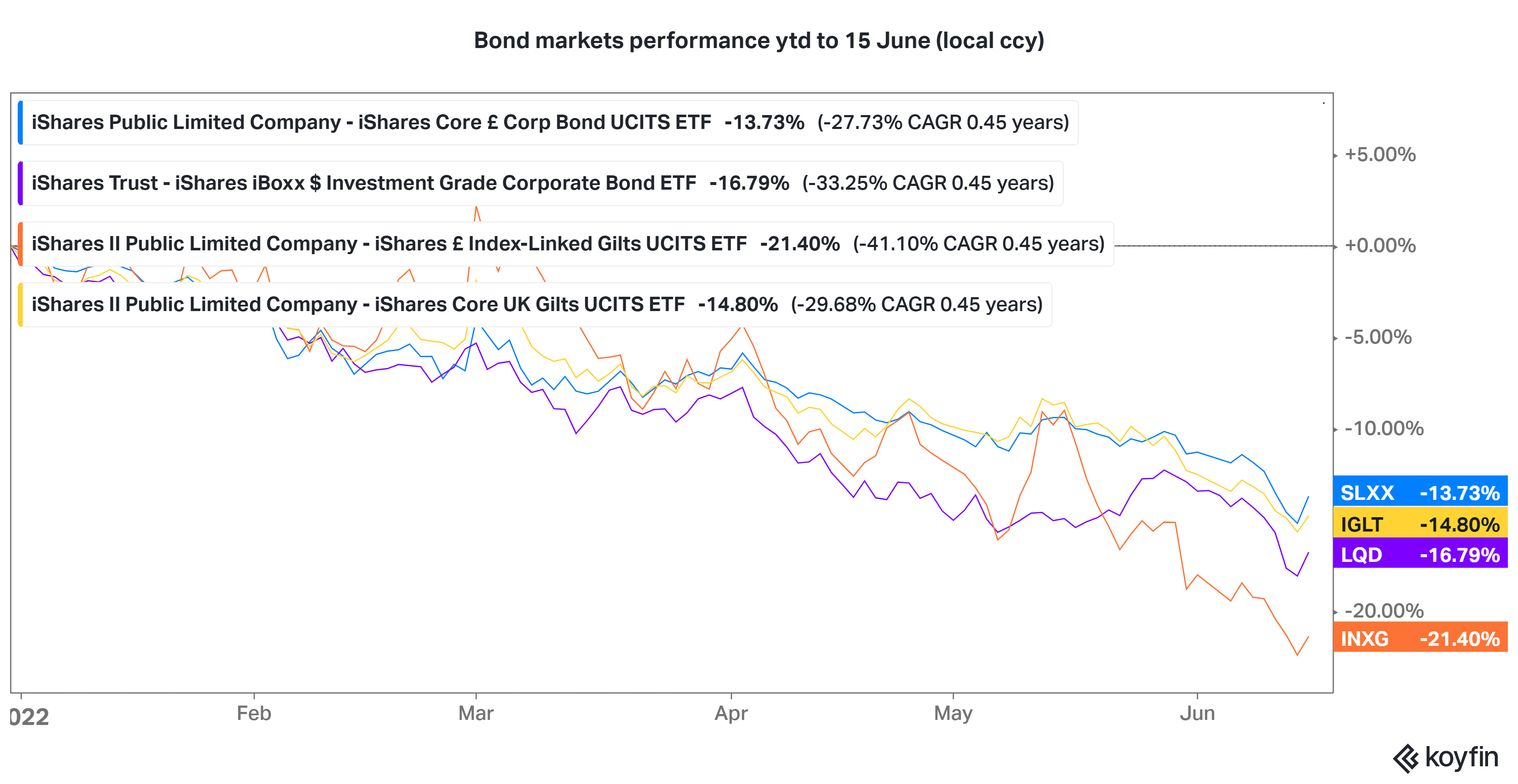

Higher expectations for long term rates (again, again) sent bonds lower (again). Look at those index-linked gilts, almost lost as much as equities this year - not exactly inflation protection amid the worst inflation for 40 years (yes, I know why, so don’t start).

New kind of chart just dropped - the Medusa chart also known as the hairdryer chart (a technical term I’m told, but loving whoever is coming up with the names these days) is becoming an important staple

3 things I’m reading

Don’t just sell: **Socially Responsible Divestment. Three leading academics (**Alex Edmans (London Business School), Doron Levit (University of Washington), and Jan Schneemeier (Indiana University) have created a neat model that anlyses the “channels” through which investor action on companies can create real world impact, through direct action, consequences and incentives.

They conclude that in most situations a tilting approach which permits allocations to leaders in all sectors - and so creates positive as well as negative incentive - ought to be preferred to a blanket exclusion approach.

“These results suggest that exclusion may be optimal for industries such as controversial weapons, where it is relatively difficult to reduce the harm produced. In contrast, tilting may be preferred for fossil fuels, where managers can take corrective actions such as investing in clean energy.”

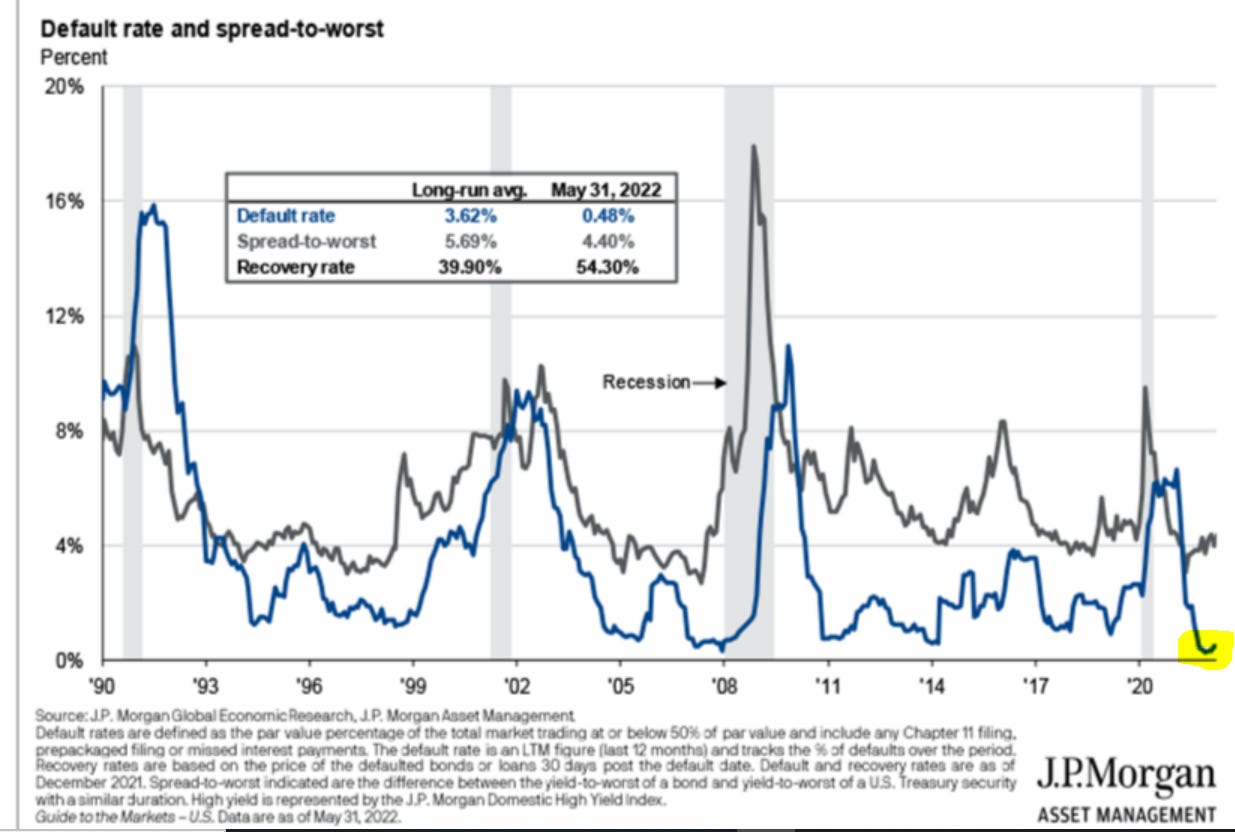

2. Defaults - where have all they gone? One of the standout charts to me of the latest JP Morgan guide to the markets (link here) was this one on defaults which are pretty much at all time lows. Not surprising when companies have been able to raise debt at super low interest rates

At the same time Jim Reid over at Deutsche Bank is out with their annual Default study asking whether we could see a return to 10%+ defaults, driven by recession, inflation and a reversal of some of the central-bank posture of the last 20 years.

For more check out my tweet thread on key takeaways from the Guide to the Markets.

3. That China Question. Jason Hsu is writing very useful things about China on his Linkedin newsletter. I wouldn’t usually feature two pieces from the same person (see podcasts below), but Jason has been busy.

Setting aside current market volatility I think one of the biggest questions global investors should be grappling with is how to invest in emerging markets and China specifically. It’s gone from nowhere to all the rage to “uninvestible” according to some due to a combination of the sketchy offshore shell entities used like ADRs , autocracy, human rights worries, direct government intervention in certain sectors and property market issues.

In the piece Jason examines various common arguments for allocating to Chinese on-shore stocks, finding that arguments about GDP size and GDP growth are weaker than commonly thought, but better reasons are around index inclusion, diversification and the potential for alpha.

2 things I’m listening to

Jason Hsu on The Compound and Friends- this was a really superb listen on a whole range of topics, with some good pushback from the hosts that brought out some great discussion. (web | apple)

The Compound and Friends: Zombieland on Apple Podcasts

Particular point of note: you can’t “buy” GDP growth as an investor. The data doesn’t support high GDP growth countries being good investments. GDP growth just doesn’t come through in earnings per share for listed entities, which is what needs to happen for investors to make money. Either there’s too much dilution, or the “wrong” kind of companies list or it’s all priced in when they list.

Doesn’t mean there aren’t some exceptional listed compaines there that can be found and invested in, but that’s a different point to the GDP growth argument.

The Long View: Cliff Asness: Value Stocks Still Look Like a Bargain on Apple Podcasts

Cliff’s always good for a listen, my two key takeaways from this were:

He reckons value stocks remain vastly undervalued relative to growth, even with the move we’ve seen this year.

He summarised some of his thoughts on illiquid investing which I think are closer to the mark than many would like to admit: do investors in fact overpay for illiquid assets because they carry the benefit of hiding the true underlying volatility, which in turn makes investors more likely to be able to hold them over a long time period. Food for thought. I think this is more true than most allocators, consultants would like to think.

Related: excellent twitter thread on investing in public vs private companies from Drew Dickson (here)

Bonus froth -

How what we eat drives so much of our economy and what’s around us. Fast vs slow food, the economist asks (web | apple). What’s the most underappreciated thing about investing? We’ve asked this question of nearly 100 podcast guests now, some answers might surprise you.

Seen last week - where do you stand on doggie ice cream ? In or out?