The Gilt Shock

The Gilt Shock

Elephant in the room, peak pessimism, cash is not trash, why we like stories

Hi folks, particularly all those new readers this past fortnight!

I could give you my usual waffle this week, but it’d rather be dodging the elephant in the room wouldn’t it … (If you’re done reading about LDI this week jump to halfway down)

As you’ll all know by now last week LDI programs faced yields surging higher further, and faster than what they had been designed to cope with, and this caused a serious market event.

I don’t think anyone went into work on Friday 23rd September thinking that LDI was days away from being in a state of such fragility, but here we are. For what its worth, I do agree with what Kerrin Rosenberg has been quoted as saying that by last Wednesday morning we were in a liquidation spiral, the logical conclusion of which absent intervention was most levered LDI positions being stopped out. Now, thankfully, that didn’t happen.

I’ve written on the history of LDI here (the FT also ran this in Alphaville: go for the article, stay for the comments), but in brief and as many folks will know, it’s a risk management tool designed to protect pension scheme funding levels and deficits, which are two things that DB pension funds have come to care a lot about. Yes, it uses derivatives.

Some folks looking with the benefit of hindsight will use words like “always” and “never” when it comes to anything involving derivatives. I prefer not to use those words when it comes to markets, I don’t think anything is inevitable. Yes, good ideas can be taken too far, this is a real problem, and with derivatives it’s always a question of degree: 1% leverage makes no difference, 100x leverage on almost anything is a disaster waiting to happen. So what’s the right level? That’s the key question.

It's important to get in context the size of these moves we saw last week. They were epically big by any measure. But you don’t want to have all the unself-awareness of a Goldman’s CFO un-ironically moaning about the impact of 25-sigma events, two days in a row.

I think the industry needs to have a measure of humility and introspection about what happened, and be open about things. Not cultural traits/norms that are as common as they should be, I’d say.

As is so often the case, many of the key questions to ask relate to our own behavioural tendencies.

Joe Wiggins provides a useful behavioural framework for thinking through a lot of this. Quoting some of Joe’s key points, which are all important principles worth remembering;

Both financial and mental models can break under stress

Predicting when things will happen is close to impossible

Markets are about the behaviour of other investors

Small sparks can lead to great damage in complex systems

The availability heuristic says that we tend to base our judgements on situations that can be readily brought to mind and this is a key behavioural issue in a changing world. We’re now in a different environment to the last 10 years and need to adapt.

When you’ve had a period of stability, a lot of the features of that get very familiar, investors become conditioned and it can get built quite deeply into how the industry operates, and even unconsciously make their way into the beliefs of those designing programs. It can become foundational to how newcomers learn about the industry.

We don’t deal well with evaluating low probability, high-impact events. We’ll either tend to completely disregard them, or attach far too much probability. This means that scenario tests of extreme things, even if they exist, are often not internalised properly or aren’t actionable in any useful way. It’s like, yes you could have shown a scenario test of a 400bps rise but would you have really taken it seriously (be honest!) and what would you have done? This one’s particularly tricky I think.

Probabilistic models only get you so far, so don’t fall in love with them too much.

So what does it all mean:

Access to levered LDI has been basically “built in” to scheme asset allocation design for years, this was sensible at the time but probably needs to change (and has significant consequences). Pension funds will have to reckon with a steeper trade-off between risk management and returns going forward - they may need to go for less hedging or less returns. Where they are looking at growth assets, liquidity is probably going to be key. This has quite a lot of knock-on consequences for the £1.5trn asset pool of private sector UK DB.

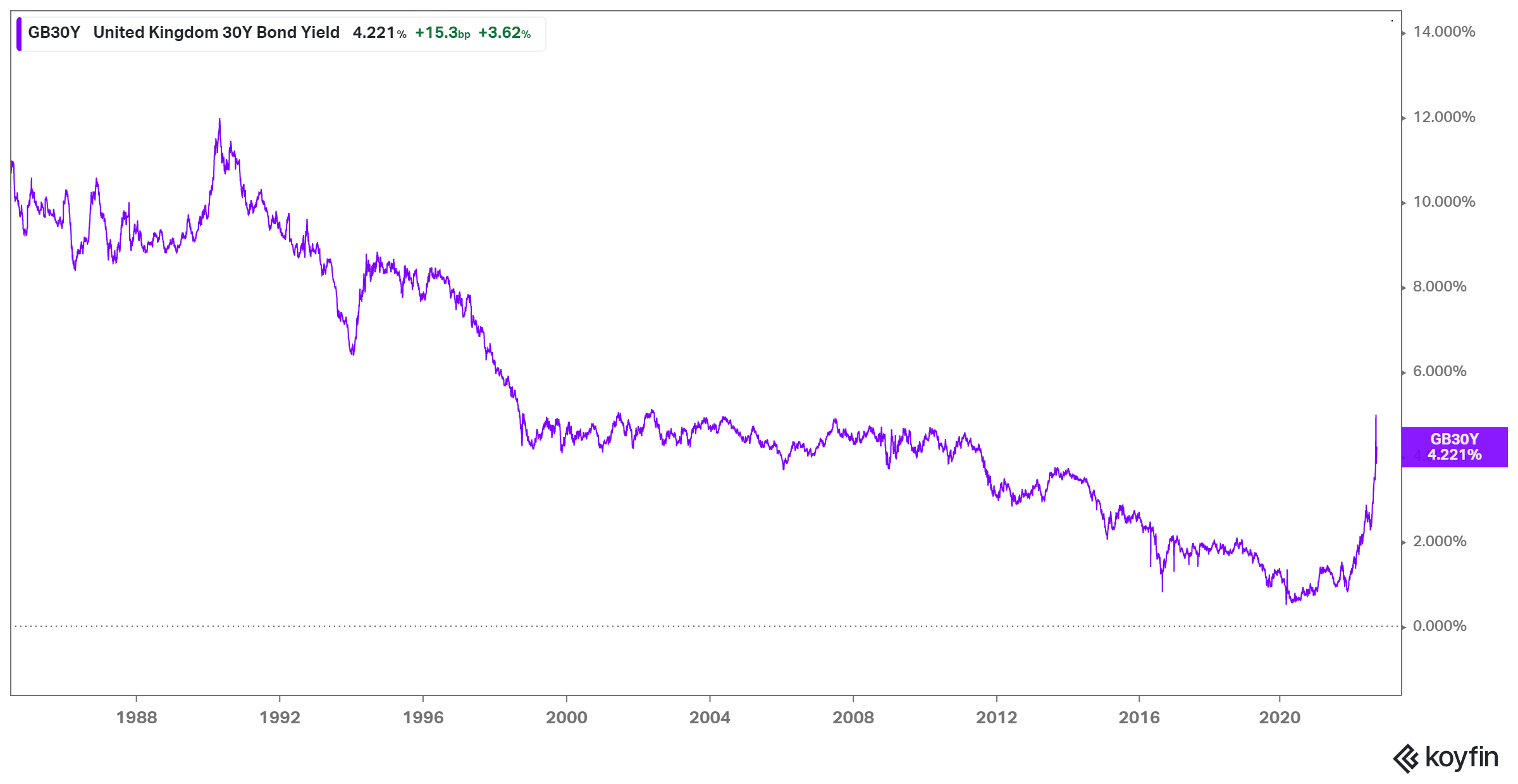

This is where it leaves UK 30-year rates at compared to the long term, this year has seen a hell of a re-rating from where we’ve been

Right, in other news, markets.

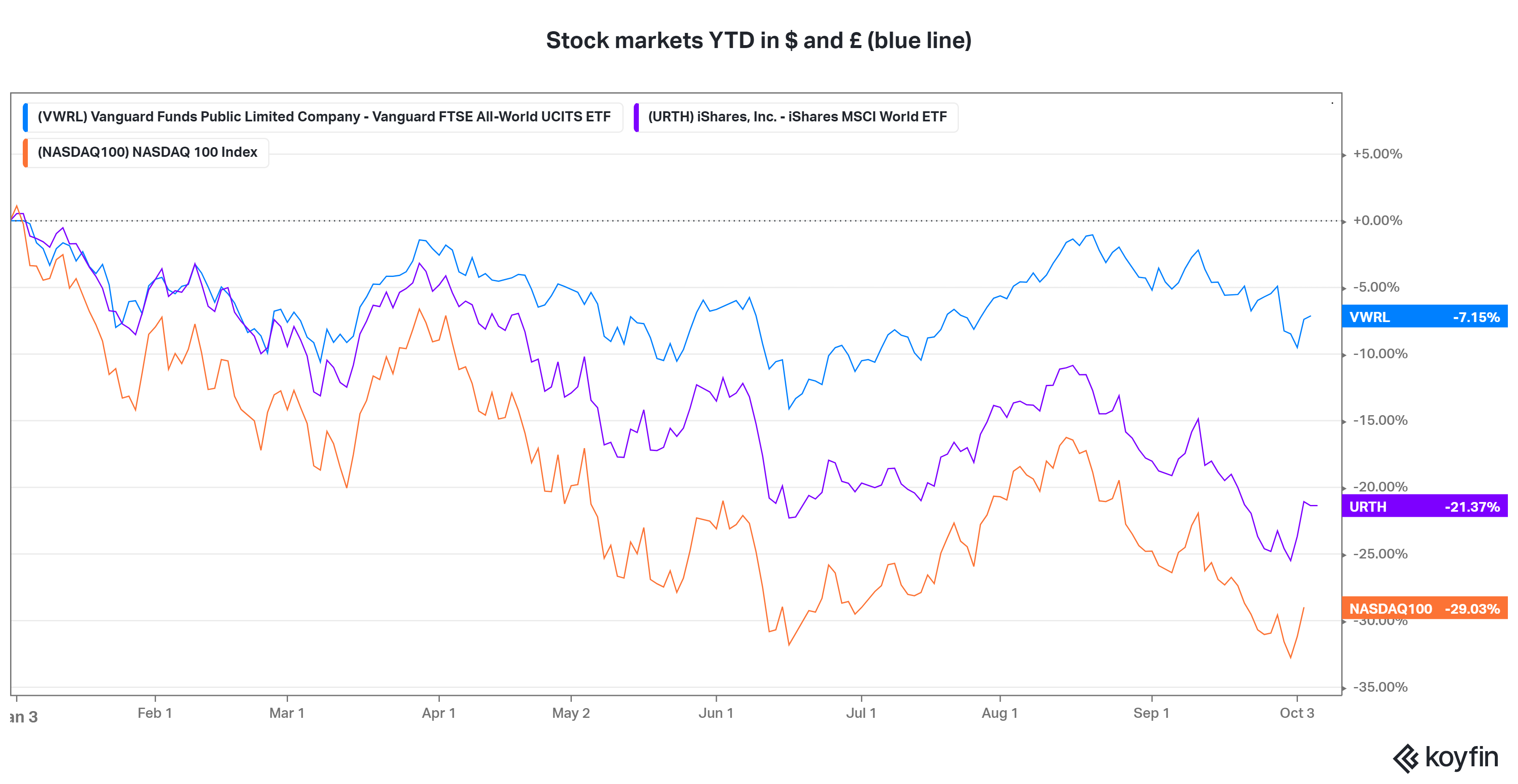

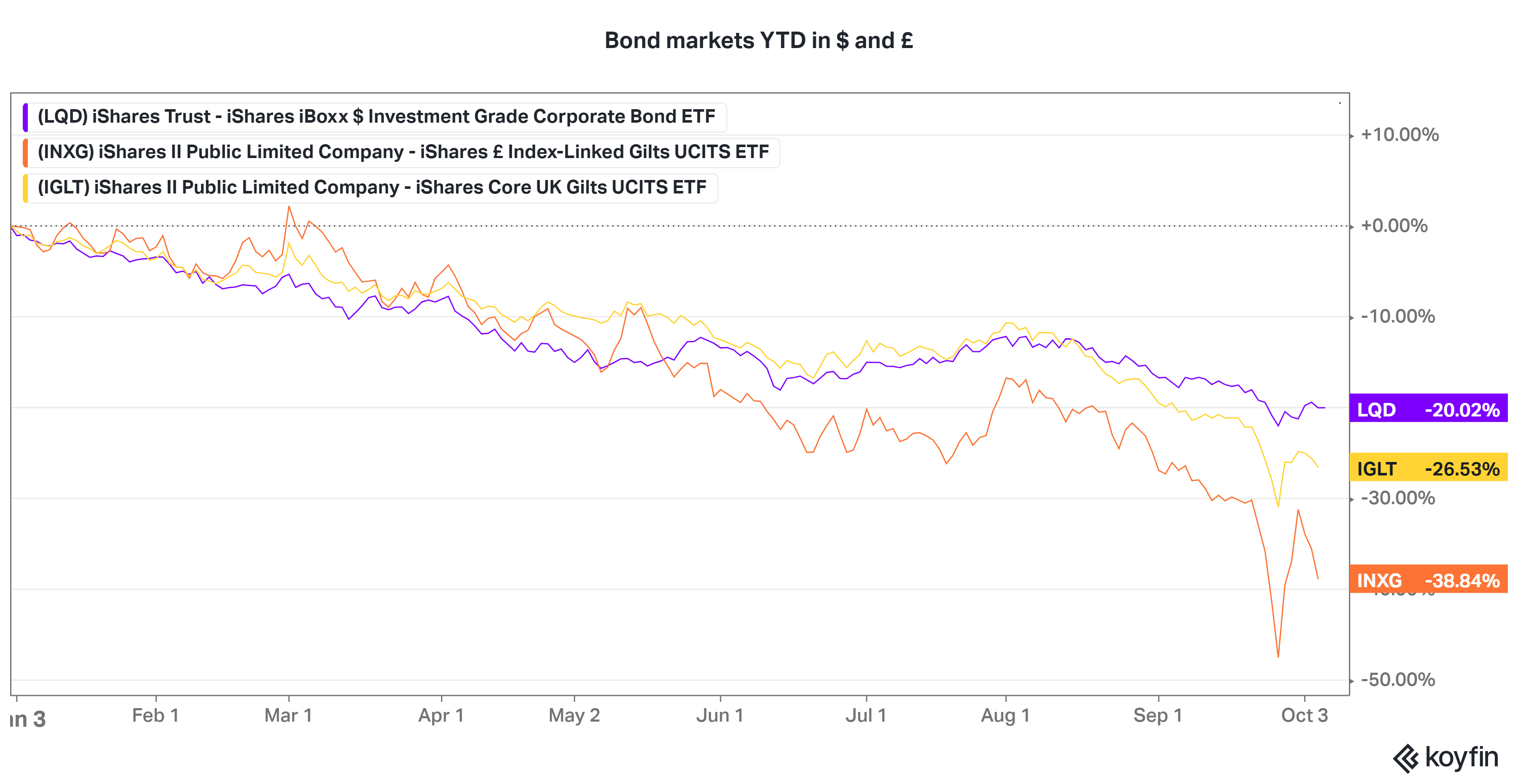

It's been a rough fortnight in markets more generally as stock and bond markets hit new lows for the year at the end of September, before bouncing back just a touch in the last few days. It's all the usual Fed mumble, “pivots”, and a bit of "bad news is now good news" type thing. At one point last week the index linked gilts were down 50% for the year.

If you're looking for a reason to be positive, with so much consensus pessimism around the Fed driving a recession, much of it surely has to be in the price here. The latest Animal Spirits ("Long Term bullish") is worth a listen with Michael and Ben (web | apple). They make the point that whenever stocks are down this much, future returns over decent time periods are usually pretty positive.

If you want something a little different to get into check out our episode on the future of the energy market with Andy Bradley. He makes the great point that a decentralized, renewables based grid is fundamentally very different to a fossil fuel based system, and we’re just at the start of getting to grips with that. I learned a ton from this on one of the big issues of the moment. (web | apple).

My reading has not been what it usually would be these last few weeks, but a couple other things that caught my eye:

Ray Dalio says cash is no longer trash - the interest rate available is now about right he says (Ray just got the end of TINA memo)

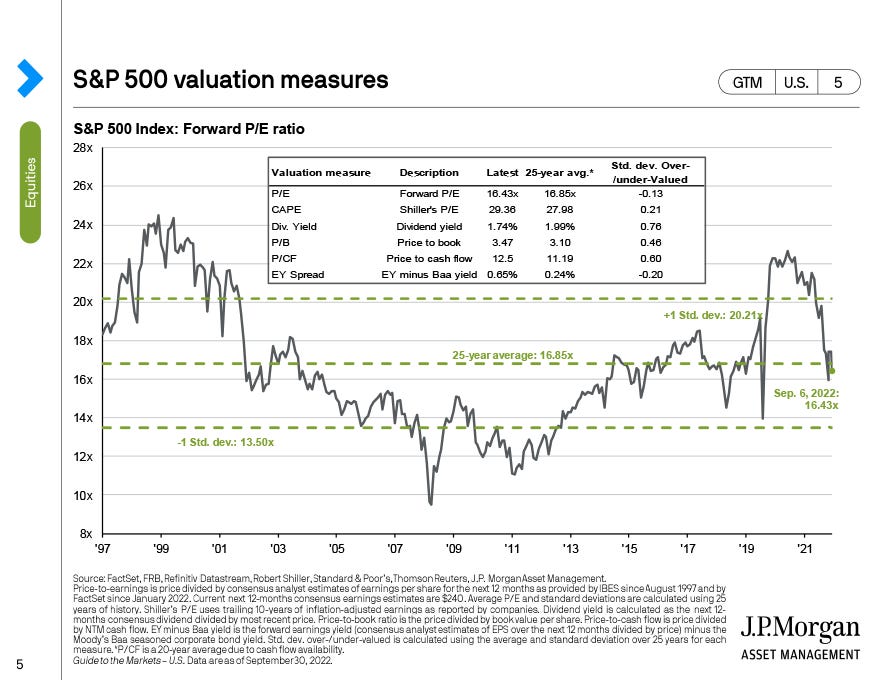

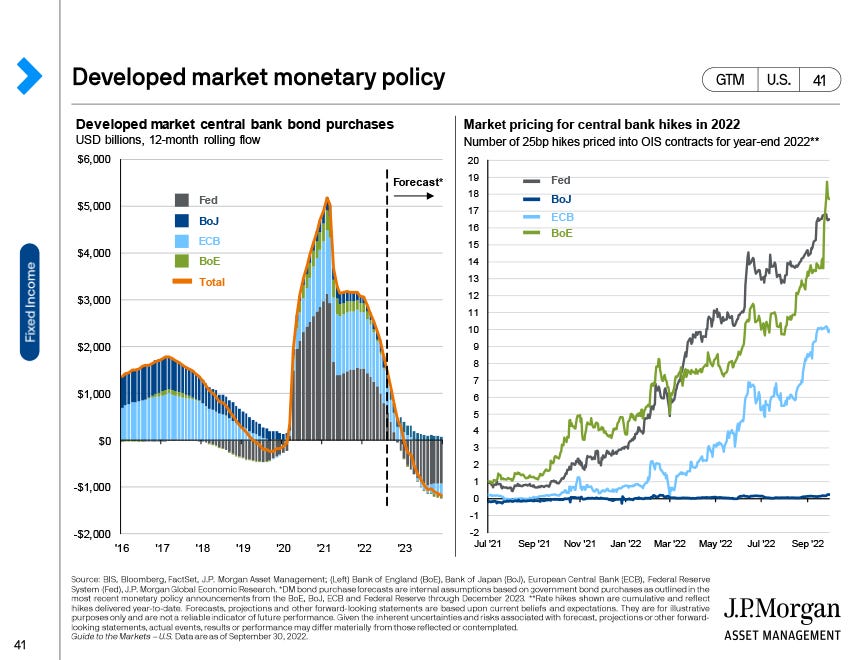

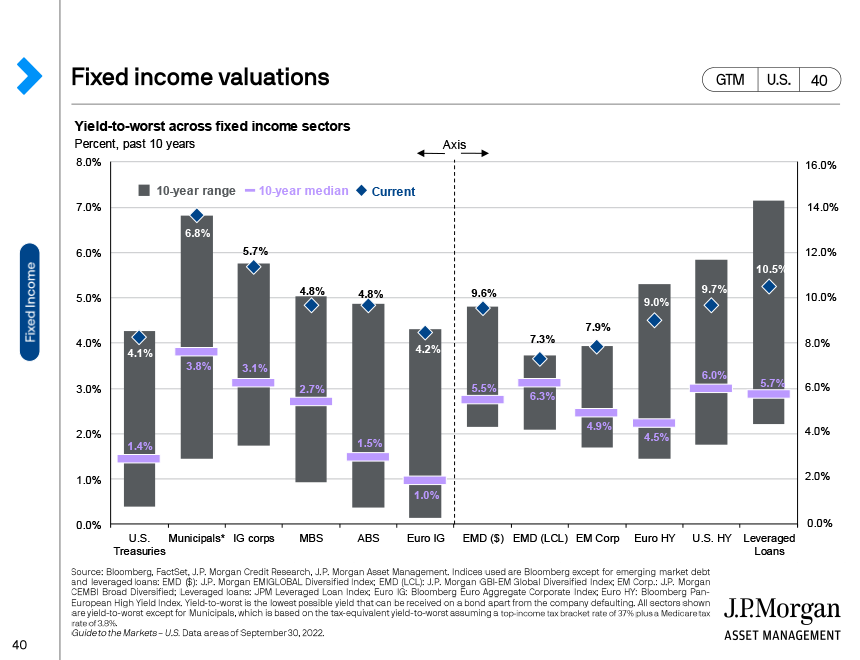

JP Morgan are out with their end-September chart pack. Notable data points on the equity market price earnings ratio (roundabout long term averages), surging expectations of interest rate rises (still! And look at the UK) and sky high yields available in corporate bonds

The Standard Deviations podcast with Tom Morgan was really excellent (web | apple).

Some gems: There’s an evolutionary reason we love gossip - Understanding the ppl around us is/was existentially important for much of human history. “The way we take on stories … we’re drawn to narratives that download highly relevant information to us … or show us where we might be going wrong in life “

In lighter news - I need all your herb garden top tips, all of them, and I need them right now. Yes, I know it’s the wrong time of year, don’t @-me. This is what the re-launch of the herb patch looked like last week. Yes, we’re calling it a diversified portfolio (satellite allocations to Mint - separate pot and Basil, indoors).

Normal service resumed in a couple weeks. Have a great end to the week!