The January Effect

The January Effect

I'm stunned to say that a thousand of you have already signed up across Linkedin and Substack to receive these updates. Thanks so much for the support, I shall do my best to make it worthwhile (and if you really like these, do please recommend to a someone else you think could benefit from it).

On to this fortnight's update - powered this week by the Columbian roast

The market is expecting so many hikes this year you're going to need a new pair of walking boots and the stockmarket does not love to see it. Also, geopolitical risk.

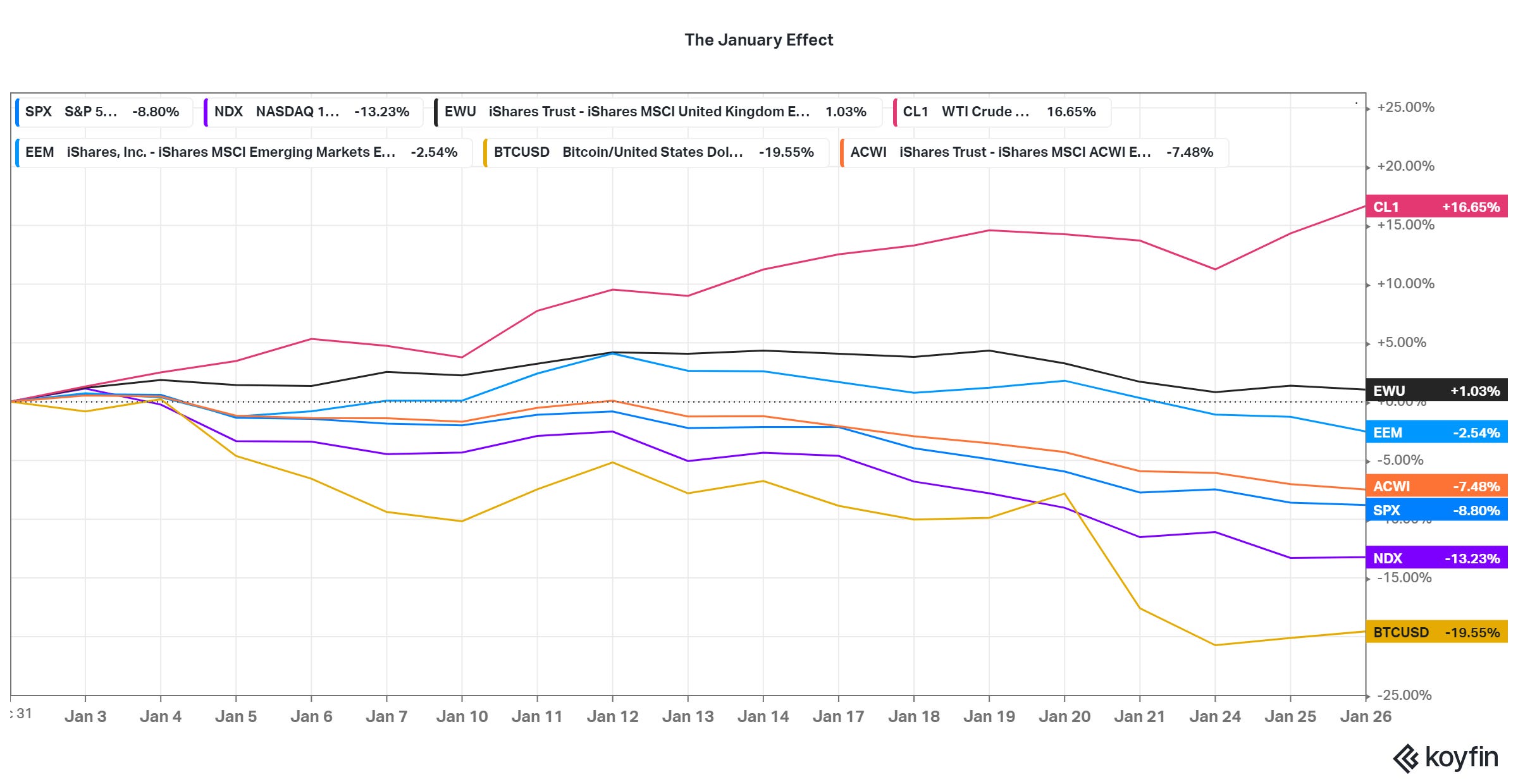

Long crude short bitcoin. TFW crude oil (+17% ytd) is more than 30% ahead of bitcoin (-20% ytd, -44% from last November) tells you all you need to know about the market so far this year and most stocks/indices sit somewhere on a spectrum between those two. Interesting that Bitcoin trades more like an exaggerated version of a speculative tech than gold or other safe haven. There's also yesterday’s Fed presser, and earnings season just kicking off, the usual mumble. So far earnings are a bit meh save for the banking sector which broadly creamed off a stonking set of revenues from 2021 trading & IPO activity (sorry for the technical jargon). For the play by play on these check out John Authers recent columns here and here.

The net result is below, with UK stock indices still on top (we love us some bankers and oilers).

Net result is the stockmarket has already fallen much more than it did at any time in 2021, but in-year 10% falls are very common, happening two years in every 3 (Ben Carlson writes). So, nothing to see here.

Three things I’m reading

Larry Fink's annual CEO letter is one of those things where it's better to read the reactions rather than the piece itself. ESG activists basically said it was more blah blah and sleight of hand that supports the status quo and lets the industry feel fine about doing nothing different. Traditional freemarket types responded by saying things like "don't make our companies waste resources on this rubbish" and, does Mayonaisse really need a purpose (thanks Terry Smith for that one). The letter is fairly long, but the important bit can be summed up by "stakeholder capitalism isn't being woke". Of course, we all know he isn't really writing to companies at this point is he, it's clients and potential clients.

The risk at this point is too much data, too little information. More data is not always better says Aswath Damodaran in his custmary January deepdive into stockmarket data from around the world. His site is great, a couple of takeaways for me this time around were: he reckons 45% of total global listed market cap (47,000 companies) is in the US (which means common indices actually overstate this at the expense of China and other Asia), he assesses the forward looking S&P500 risk premium at 4.2% p.a. using consensus earnings estimates fairly middle-of-the-road compared with history, so equities fairly priced (and that was before this month's selloff)

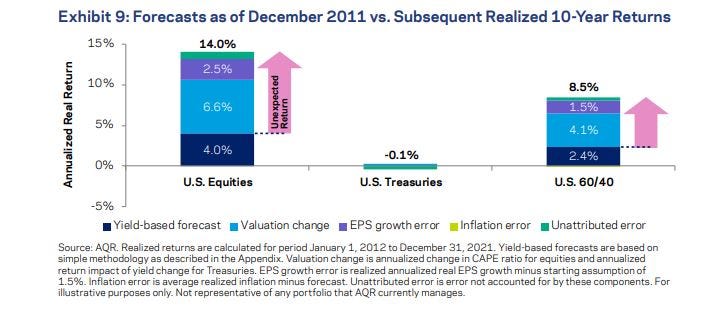

Watch out for those unexpected returns. AQR are out early with their updated long-term return assumptions. The headline is that the real expected returns on a 60/40 portfolio hit new lows around 2%p.a. But the real (pun intended) story here is not on the "60" but the "40". almost all flavours of bonds, even corporate bonds and even high yield are now at pretty much zero real returns, negative after fees. I also tend to follow Blackrock, JP Morgan and GMO's assumptions, we'll see where they come out. Mea culpa issued for decade old forecast of lower returns - in 2011 they forecast expected real returns of 4% per annum. the outcome? 14% per annum. a full ten percentage points of un-expected returns every year.

Two things I’m listening to

The Compound and Friends - Intangible Value. Another regular listen for me here from the Ritholtz Wealth stable, but this episode was an absolute standout with Kai Wu. Intangible assets (eg brand - think:Nike, know-how - think:Boeing, networks and code - think:google, facebook) are taking over the world but accounting measures (eg earnings, book value) don't do a good job with them. This has posed a problem for stock valuation and knocked a hole in a many a value manager's track record. Here podcast guest Kai explains how to think about this (Apple).

Health. I've been wondering a lot recently about the connection between investing and health (bear with me here). I think there's more there than you might imagine, and might even be a big trend over the next decade. This podcast sums it up nicely.

(Apple | Spotify)

Bonus froth

WFH is over - at least in the stockmarkets anyway. Pandemic era winners like Zoom, Peloton and Netflix are back trading at levels they were at BEFORE covid hit. Bellweather growth funds like ARK innovation ETF and the Scottish Mortgage Trust have given up much or all of their pandemic-era outperformance .

Ozark season 4 is here. Enough said.

What's the most effective communication medium known to humankind? STORIES. On our own podcast these last two weeks we’ve had Stacy Havener who has helped boutique asset managers raise $billions breaking down how to tell better stories in a business context - essential listening for anyone who does any sales or marketing (Apple | Spotify) , and last week we had professional trustee Robert Thomas helping us deconstruct what works in board meetings and top tips for advisers working with trustees (Apple | Spotify )

And one thing to brighten your day

What Americans think a Finnish workday is like - from the content geniuses at Morning Brew

Have a great end to the week, see you in 2 weeks