Unbothered

Unbothered

Bbq season, runs, tilts v overlays, the Romans, datacentres & going transatlantic

Good morning, how's everyone doing?

A happy Thursday to you all especially my Twitter impersonator … and thanks to those of you who reported it – honestly I think I’m feeling kind of smug about the whole thing. Not to brag. No big deal.

But you know what's even more exciting than having a fake Twitter account? The BBQ course I went on last weekend! Let me tell you I learned all sorts of fancy techniques like direct vs indirect cooking, using a smoker box, and cooking to temperature (48 degrees for a medium rare Tomahawk steak, since you asked). We even did an afterburn - now that's what I call a good time.

Let's just hope this weather holds up so I can give the new skills a proper rollout.

In a boon for headline writes this fortnight, the company behind everyone's favourite kitchen staple, Tupperware, is in some hot water. Apparently its fate is sealed.

Macro mumble - the worst continues to not happen

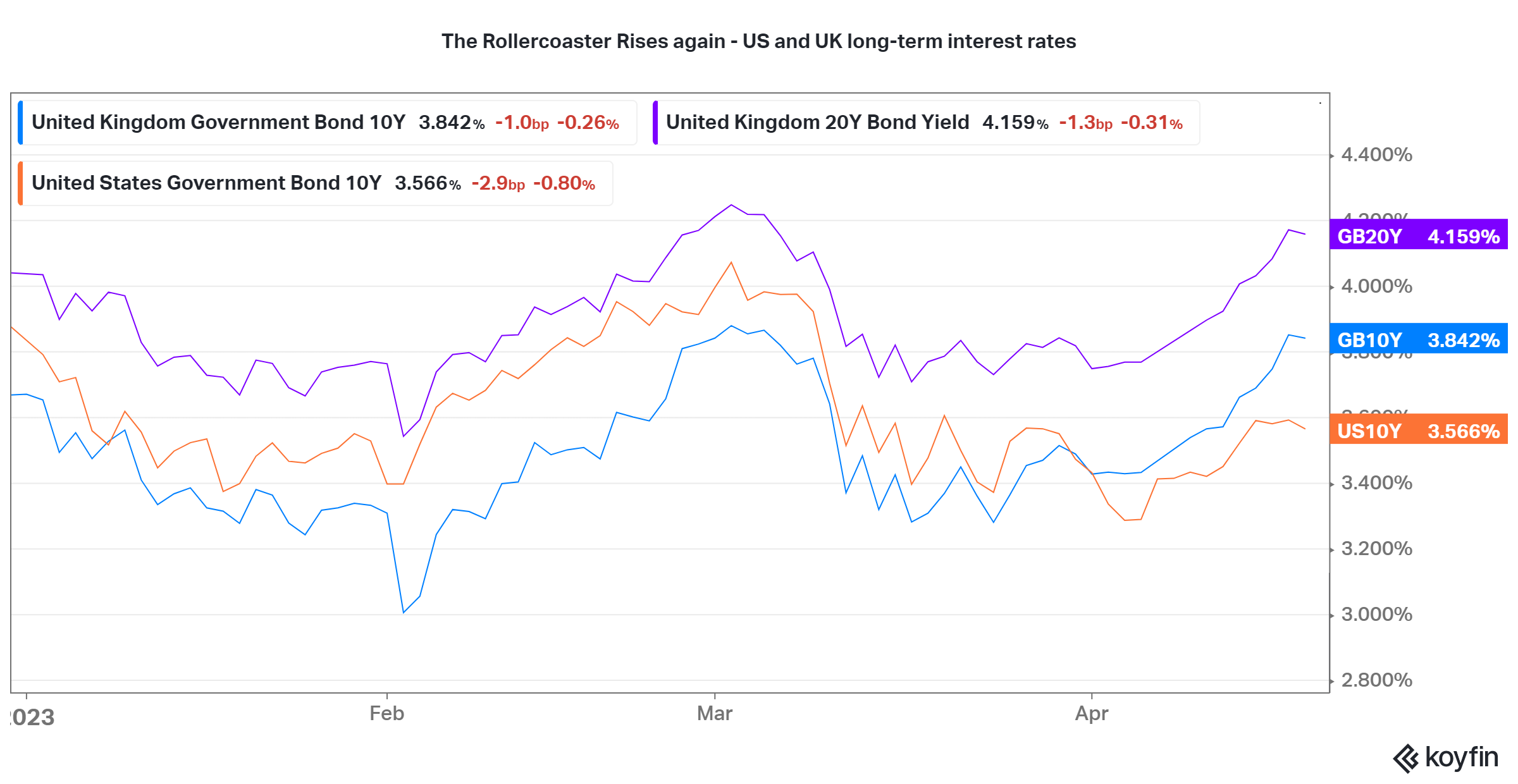

Now, for all you macro mumble lovers out there, it's time for the market update. Data out of the US has been behaving itself better than a toddler in a candy store these past couple weeks, causing no big surprises. Inflation has been falling, labour markets are easing up, and 10-year interest rates have been slowly creeping higher. Stock markets are generally unbothered.

With the biggest chunk of US inflation now coming from the lagged shelter component, some commentators who replace these measures with more real-time data even think that US inflation could be getting within shouting distance of target.

There’s still at least two schools of worry - that the Fed might tighten too much, or that a recession is already on the way leading to earnings falls. But for now the data is sort of just-right, many investors have positioned for the worst but the worst continues to not happen.

The picture in the UK though is a little different. This week’s inflation print was higher than expected, with CPI remaning above 10%. On the face of it that’s far stickier even than other comparable countries with similarly high peaks (like Italy). Why? Soaring food prices (19% inflation) is one answer, but the other is energy markets where the UK has a slower pass-through of lower wholesale prices. We need to see the big price cap hikes of last April and October work themselves out of the numbers. When this happens large falls are expected.

Yes but, core inflation in the UK is proving stickier than elsewhere. An alternative viewpoint is that the UK typifies some of the challenges of this cycle: growth slowing but not enough to stop inflation. High interest rates but stubbornly above-target inflation.

I love it when a new kind of chart drops …

For one view on this transatlantic difference I instantly loved these charts even before I knew what they were saying (giving strong “floorplan of a caravan vibes” - thanks Tess) Source Alistair Winter, Joe Weisenthal

This has meant yields on 10-year gilts creeping up above yields on 10-year treasuries, in a reverse of the positioning for most of the last decade (chart below). Some think that’ll have to go further to get gilt supply/demand in balance in world where DB pensions are no longer bulk-buying gilts.

Markets -

Stocks are unbothered, the spring bounce has taken global markets to up 9% YTD in $. Non-US markets are having a moment (+12%) while EM is behind (+4%). The rates rollercoaster continues but at a more sedate pace

Interest rates - note the crossover of gilt yields vs treasuries

AGM season is underway, and it’s looking interesting already with pension funds being more vocal than usual with an article in the Times on 5 schemes planning to vote against BP’s chairman, and health-focused shareholder proposals at Nestle also making the news.

Three things I’m reading

Tilts vs Overlays: Newfound Research [link] - warning: geeky

Very neat piece that hits on a few useful insights:

The dilemma: You might find “good assets” that do well when stocks do badly, which ought to be a good thing but, if they return less than stocks you create a long term drag on your returns in allocating toward them. This is called the “funding problem”.

A solution (1): Overlays solve this in theory (and potentially in practice, some of the time).

Also, an overlay is a helpful mental model for almost any tilt away from a benchmark. That can be extended to think more directly about active share, which gives you a framework for analysing the performance hurdle needed to overcome an active fee load.

The solution (2). Overlays aren’t always available in practice, but anyway optimal portfolios use a mix of overlays and tilts, as this neat chart shows

Yes, but: I think there are behavioral reasons that complicate the picture quite a lot here. An overlay works in theory but much less in practice when it gets very painful rolling a money-losing position each year, whereas holding on to an underperforming long position is less bad. So I think this leads you to prefer tilts to overlays, slightly more than the pure quant work would have

And finally … you gotta give credit to author Corey Hoffstein for this gem: “Nevertheless, over the long run, on a log scale, drawn with a large enough crayon, and if we squint, we see a very similar picture.”

I’m here for large crayons and log scales.

The Romans - what did they do for us: Empire State [The Actuary Magazine - link ]

George Maher concludes that Rome grew, prospered and died due to motivations and behaviours that are little changed from ours today. Can we learn from its story?

Neat little explainer on the Romans and economics - it took 1,000 years for Europe to return to the same level of quality of life and trade as at the fall of the Roman Empire.

It was an economy based on growth (and of course conquest), but the expansionist drive was also behind the eventual fall as well as currency debasement, complacent populations, sidelining of institutions and bad leadership.

Who owns Kent? (link)

Thought provoking piece previewing a new book that questions the benefits of the new asset-managers-own-the-world situation that we may be creeping into, unknown to many folks in the wider world.

Two things I’m listening to

I’ve been picking up the running again now mornings are so much nicer with an eye on a runout at one of the Spartan events over the summer, and I do find a good podcast really hits different on a run! These two really stuck out:

I mentioned Commercial Real Estate briefly last time - and that while there’s probably bad news out there it’s also probably priced. Maybe not says Jim Chanos here (and yes I know he’s a short seller and talking his book) it’s a well thought out case and should give any investor pause for thought and to ask a few searching questions on what is often put forward as quite a trendy new area of real estate or infra investing.

Like a lot of folks I’ll admit to have been on a bit of a journey with Taleb. Ate up his first book “Fooled by Randomness” circa 2007. Got lost and bored during the followup “Black Swan”. Never quite got “antifragile” in the same way. Got quite put off by his general nastiness on social media and condescending attitude.

Anyway, this interview is a lot better than expected, he’s at his thoughtful best talking about why tail events drive so much in the world, why expertise matters in some domains more than others and why he now roadbikes as well as deadlifting, plus lots more. It’s worth a listen. Plus, they have a cool new logo

Bonus one - I really didn't expect that the most thought provoking finance / economics podcast I heard last week would be from .... Jonny Wilkinson, but here we are 😁 Interview with Jennifer Hinton, our relationship with profit (link).

Grab bag

Succession season 4 is all I’m going to say. omg, iykyk. No spoilers please.

Guessed I’m a little bit obsessed with research and data on time use so I jumped at this headline …BURNT OUT BRITAIN: HOW WE USE AND MISUSE OUR TIME, AND WHY IT MATTERS [ report - link ]

The bottom line: More people than ever are burnt out, but the common diagnosis is wrong and fails to address the causes. No we aren’t working more, no we aren’t sleeping less. But our days are more fragmented. Time confetti is the problem.

Returning to the transatlantic theme, apparently: The Americans are coming ….

Morning Brew writes:

Whether it’s to manifest a White Lotus Sicilian adventure or protest at Credit Suisse’s headquarters in Zurich, the number of Americans planning to travel to Europe this summer has skyrocketed. Kayak reported that searches for European travel are 77% higher than last year, and Hopper said that of its US-based customers browsing international destinations, 37% are searching for flights to Europe.

Surging interest in transatlantic flights is a California-in-1849-level gold rush opportunity for airlines, and they’re scrambling to increase capacity to meet demand.

Yesterday, JetBlue announced a new route to Amsterdam from JFK that will begin in the late summer.

United has tacked on nearly 25 international routes to this summer’s schedule, including additional flights to Barcelona, Berlin, and Naples. The airline will be flying almost two dozen flights daily from the US to London Heathrow.

Croatia’s Pula Airport is even considering lengthening its runway to accommodate bigger planes that fly across the Atlantic. Currently, the country only has two transatlantic flights.

I’ll leave you with a couple of snaps from this morning’s run … have a great day