Out of Office (OoO)

Out of Office (OoO)

It hasn't peaked, expected returns shoot up, Sri Lanka, freedom weighting & soundtracking your summer

It’s got that “thanks for your email, I’m back on …” energy right now hasn’t it? If we aren’t sweltering in our back gardens here in the UK, or wondering if we still have a government we’re getting our OoO on and getting out of here. What’s your preferred OoO message style? Minimalist? Smug? Comprehensive? Unexpected? Let me know your tips in the comments

It’s still a few weeks till the Mikulskis family decamp to the banks of the river Charente in south west France for our annual summer trip, so I’ll keep things going until then at least for all of you keeping the wheels turning here.

We’ve been busy on our podcast getting out a couple of final episodes before breaking for the summer and we were so stoked to get Michael Mauboussin himself on for a long chat on investing frameworks, thinking about valuation from first principles, what “consilient” actually means and why there should be more of it. Have a listen (apple | web | summary).

I’m not sure whether the twitter/Elon thing is still “market” news or just belongs in the general entertainment bucket these days but still, deal’s off, it seems. And we’re all getting a good lesson in what MAE means. Derek Thompson’s here with the drilldown -

Markets have really flat-lined over the last month or so, we’re at the boring stage of the bear market. Even yesterday’s bad US inflation print didn’t move things that much even though it put a whopping 100bps (1%) potential rate hike on the table for next month. There’s been a little more excitement than normal over some of the second-tier economic data in the US, everyone is poring over the numbers trying to call the turning point or find a recesssion indicator. This week is as a big one for important macro data: inflation, jobless claims and retail sales.

I still think you can say everything you need to about the current macroecnomic situaiton in 13 words: “inflation is out of control and central banks are hiking rates like mad”

All we really wanna know is … Has inflation peaked (no), are we heading for a recession (vibes are real) and where will the Fed funds rate peak (~3.5%)?

Can we admit that most of these questions are just entertainment for long term investors though? In the fulness of time it’ll all seem obvious.

Corporate earnings season (just starting) also has slightly more import than usual for similar reasons - company earnings have been amazingly strong this year despite declining stock markets. If that starts to change then it’s news.

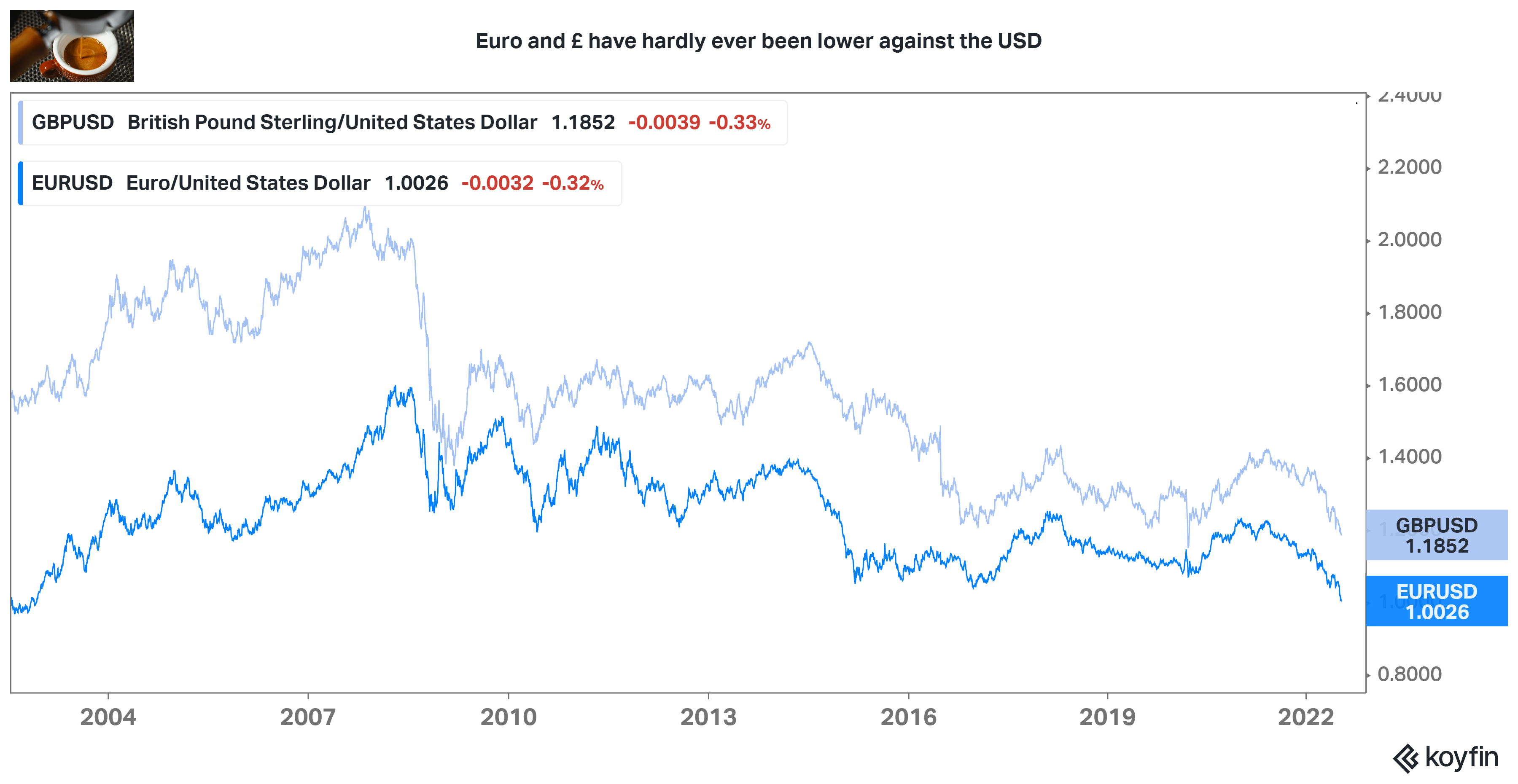

Wait but, STERLING 💷

Who knew having a government meltdown is not great for your currency!

Ah but also, watch out for the Euro - it’s not just sterling charts that market watchers are following closely this week though, the Euro is plunging vs the dollar and breaking through the 1.00 level. It’s psychological, apparently. Both currencies have hardly ever been weaker against the US dollar.

Why? The ECB isn’t seen as having as much room to raise rates as the Fed and a greater chance of recession and stagnation. With that backdrop US allocators might be wondering why they would hold anything in these basket cases.

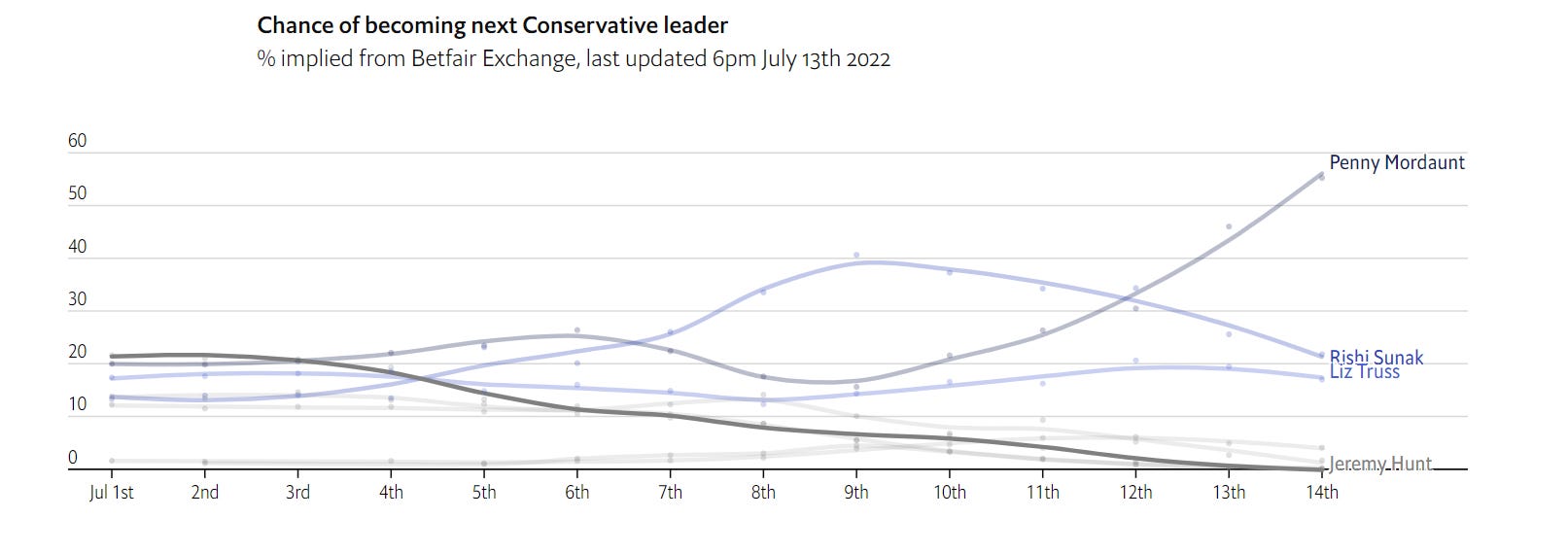

New tracker just dropped! Next prime minister tracker - The UK will have a new PM on Sept. 5. The wide field of contenders is already shrinking faster than a crypto spac, to get down to two by early next week. The Economist has the dataviz

What to really focus on here -

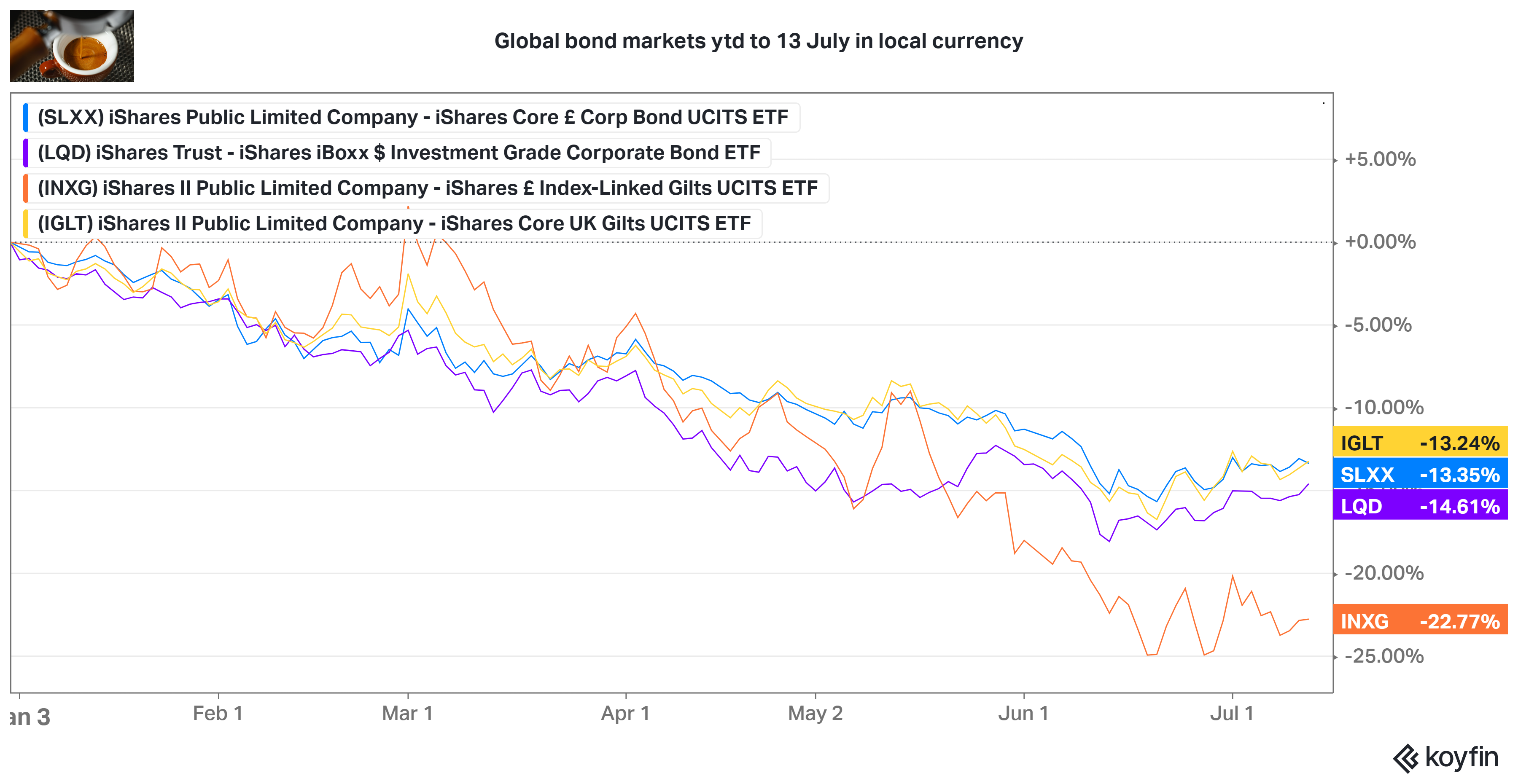

Expected returns is the thing to focus on as forecasters, managers and advisers bring out their 30 June assumptions which are sure to have shot higher since the start of the year. Professor Damodaran pegs the future S&P returns at over 9% p.a. now, compared to as low as 5% in 2021. Here are some more examples from the bond markets. Across capital markets expectations have shot up.

3 things I’m reading

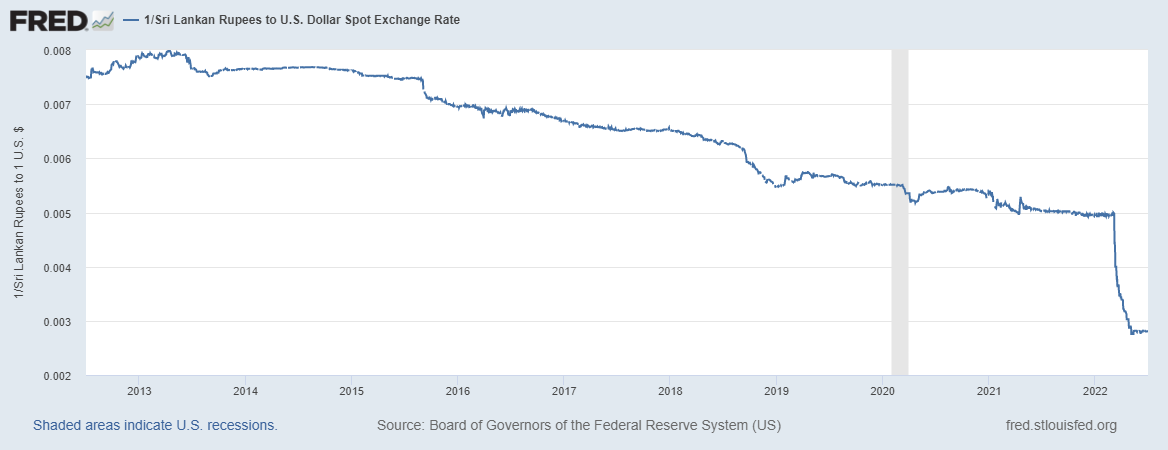

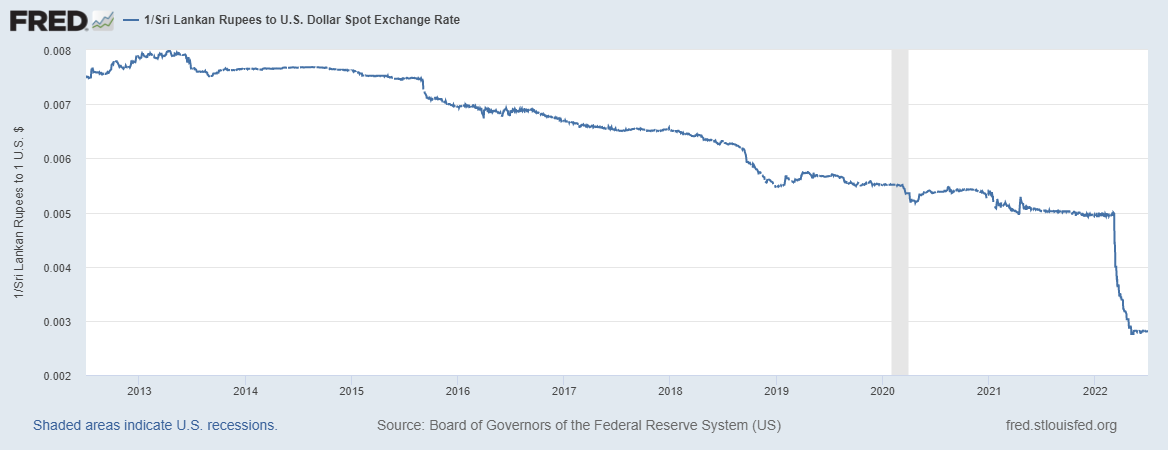

1. The story of the Sri Lanka default and why it matters - by Noah Smith (article). We’ve all seen the social media pictures of protestors storming the president’s swimming pool (which might be kind of funny if it wasn’t all fuelled by such misery and poverty) . The recent Sri Lanka default is, in many ways a classic emerging market currency and balance of payments crisis with all the usual ingredients:

Sri Lanka’s crisis features all of the standard, textbook elements:

An import-dependent country

A persistent trade deficit

A pegged exchange rate

Lots of foreign-currency borrowing

Capital flight (sudden stop)

An exchange rate crash (balance-of-payments crisis)

A sovereign default

Accelerating inflatio

One new ingredient here to be aware of was heavy borrowing from China under the Belt Road Initiative, and there were also unforced policy errors like banning fertiliser . Are other countries vulnerable? Yes - looking at some key ratios suggests El Salvador, Ghana, Pakistan and Tunisia could be.

2. A perfect storm of perfect storms. Do you get the feeling you’re hearing that cliche a lot recently? You aren’t alone say Joe Weisenthal and Tracy Alloway at Bloomberg. It’s the everything-storm from oil to grains, airlines to emerging markets to Texas Watermelons and Australian Avocados, things are not normal. How many perfect storms did your risk model forecast for this year?

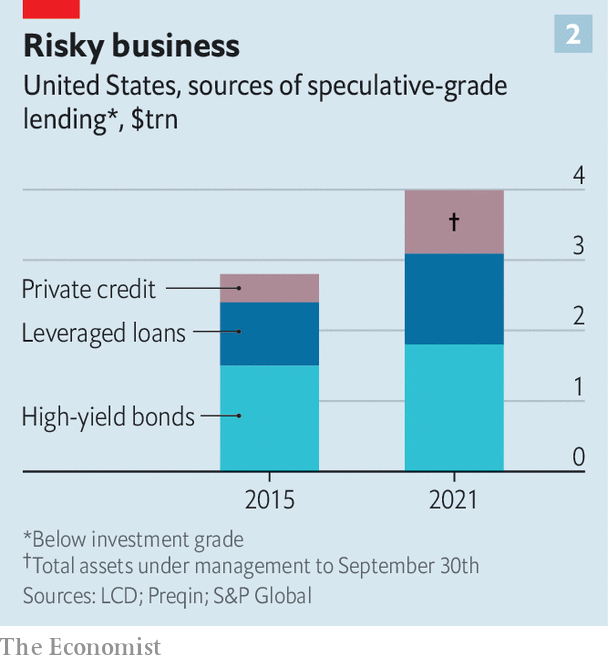

3. Defaults - can companies pay their debts?. A very common question with interest rates rising is what this means for companies borrowing money and will we see defaults rise?

We talked before about the spectactularly low level of defaults over the last year, and the Deutsche Bank forecast of a return to 10% defaults. Could the sharp rise in interest rates be the trigger?

Probably not, says The Economist (article). Companies borrowed like mad during the covid-era super low rates so have little financing needs for years. The corporate bond market has almost dried up this year and not many companies will be forced to tap the market at higher rates this year or next.

But … ( you knew it was coming) the big change in dynamic this cycle is the role of the private debt markets (see chart) whose floating-rate nature means borrowers will already be feeling the pinch. This segment has gown vastly in the last decade and the risks are far from transparent, However supporters of private markets cite the enhanced transparency and control you get as lender in this area as perhaps making it even safer than the public bond markets.

Two things I’m listening to

Acquired - lessons from over 200 company deep dives. (web | apple) Acquired is a fantastic podcast to have on your radar, the hosts David Rosenthal and Ben Gilbert do these unbelievably detailed deepdives into the history of some of the key companies of the moment including Uber, Amazon, TSMC and Sequoia just to name a few. Their 3-part epic on Berkshire Hathaway was a great companion on a long road-trip in France last summer.

This episode recaps the key lessons they’ve learnt from all their research into succesful companies and early stage ventures.

2. Perthe Tolle with Barry Ritholtz - Freedom Metrics (web | apple)

Investing in emerging markets excluding autocracies and / or tilting toward countries with more freedom (on the basis that this is necessary for sustainable long term growth) is absolutely something that investors can do now and pretty attractive given current events.

Perthe discusses the genesis of the ETF she runs which freedom weights emerging market stocks and covers some of the important questions like what data is used, how it’s rebalanced, when things change etc.

There are other approaches to this gaining traction too (eg Kempen) and I think it’s something we’ll hear a lot more about.

Soundtracking your summer

I’m quite into season-appropriate and day-of-week-appropriate music listening at the moment and the playlist search on spotify is actually great for this (just search for “spring mondays” or “autumn Sundays”) . For a bit of nostalgia the 90’s era UK summer hits also served up some absolute classics: here’s some of my top suggestions to kick of a 90’s summer nostalgia playlist: Stereophonics: Dakota, Texas: Halo, Nelly: Ride wit me, Red Hot Chilli Peppers: Californication, 4 Non Blondes; What’s Up [pretty much anything of that era by Will Smith]

Need some summer reading inspo: here are my recommendations.

Thought for the week: The days are long but the years are short - summer hard says Stacy Havener. Take that walk, have coffee outside, get the flowers, play wiffle ball …

In one thing to brighten your day Dan Toomey helps us understand how our American friends see UK politics: